For many U.S. workers, the paycheck looks better on paper this year.

Base salaries have inched higher. Some companies adjusted compensation to reflect inflation pressures from the past two years. Annual raises, even if modest, are showing up across W-2 income statements. On the surface, it appears as though earnings are finally catching up.

But the experience of receiving that paycheck tells a different story.

A worker earning $72,000 last year might now be earning $76,000. The expectation is simple: a larger paycheck should mean more room each month. Yet when the direct deposit hits, the increase feels muted. In some cases, it feels almost unchanged.

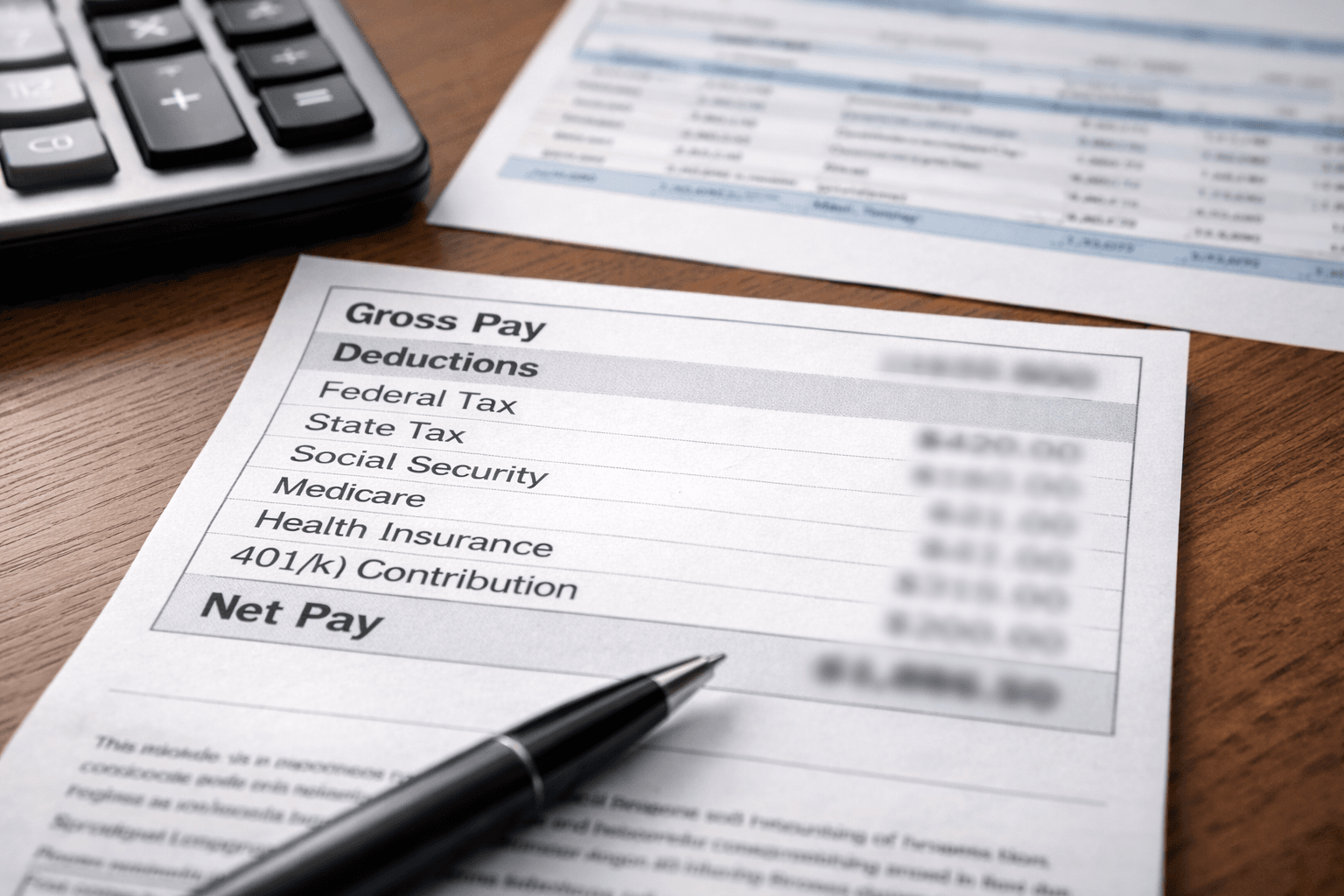

The difference is not in gross pay. It’s in what happens before the money reaches the bank account.

Withholding levels have shifted. Health insurance premiums have increased. Retirement contributions, whether automatic or adjusted, take a larger share. Local taxes—often less visible—have quietly expanded in certain jurisdictions. By the time all deductions settle, the net pay reflects a different reality than the salary headline suggests.

Over time, wage growth is no longer translating directly into spendable income.

This is becoming a recurring pattern across middle-income households.

The Gap Between Gross Pay and Take-Home Pay Is Getting Harder to Track

In earlier cycles, a raise had a clearer impact. A 4% or 5% increase in salary often showed up, more or less proportionally, in monthly take-home pay. The structure between gross and net income was relatively stable.

That relationship has become less predictable.

Between 2022 and 2025, several layers of deductions have expanded at the same time. Federal withholding adjustments—particularly after temporary pandemic-era tax positioning—have normalized. At the same time, employer-sponsored benefit costs have risen, especially in health insurance.

For example, an employee contributing $220 per paycheck toward health insurance in 2021 might now be contributing $310–$340 for a similar plan. Deductibles have also shifted upward, but those costs remain separate from payroll deductions, creating a dual pressure. A similar pattern appears in Insurance Premium Increases Are Expanding Living Costs Across U.S. States, where rising coverage costs extend beyond payroll and into broader household budgets.

Retirement contributions add another layer. Many workers increased 401(k) contributions during periods of strong market recovery, either voluntarily or through auto-escalation features built into employer plans. A 1–2% increase in contribution rates can absorb a meaningful portion of a raise without being immediately noticeable.

Local tax structures further complicate the picture. In certain states and municipalities, incremental adjustments—whether through rate changes or expanded taxable categories—have slightly increased withholding amounts. These are rarely headline changes, but they accumulate. This shift is also visible in Property Tax Increases Are Quietly Raising U.S. Housing Costs, where local-level adjustments gradually raise overall financial pressure without a single defining change.

The result is not a single large deduction, but a series of smaller increases that collectively reshape take-home pay.

Cost Layers Are Expanding Faster Than Wage Adjustments

The mechanics behind this shift are not accidental. They reflect how compensation systems and cost structures evolve over time.

Employers often adjust salaries annually, but benefits pricing operates on a different cycle. Health insurance costs, in particular, are recalibrated based on claims data, provider pricing, and broader healthcare inflation. These adjustments can outpace wage growth in any given year.

At the same time, tax withholding is designed to approximate annual liability in real time. As incomes rise—even modestly—workers may move into slightly higher effective withholding ranges, especially when combined with reduced credits or phased-out deductions.

This creates a layering effect:

- Wages increase incrementally

- Benefit costs adjust based on external pricing pressures

- Tax withholding recalibrates to updated income levels

Each layer operates independently, but the outcome converges in a single place: the net paycheck.

A worker may see a $300 monthly increase in gross pay, but after accounting for higher benefit contributions, adjusted withholding, and retirement deductions, the actual increase in take-home pay may be closer to $120–$160.

That gap is where much of the tension now sits.

How Workers Are Actually Experiencing the Shift

The change is rarely noticed all at once.

It often begins with a sense that raises feel smaller than expected. A promotion or annual adjustment doesn’t translate into the anticipated flexibility. Monthly budgets remain tight, even as income technically rises.

Over time, workers begin to notice patterns.

Paychecks vary slightly more than before, especially after benefit enrollment periods. January deductions look different from mid-year ones. Mid-cycle adjustments—such as updated insurance rates or contribution changes—introduce additional variability.

Some employees revisit their pay stubs more closely, noticing line items that previously went unquestioned. Others only recognize the shift when comparing year-over-year bank balances or tax refunds.

There is also a behavioral adjustment.

Instead of treating raises as available income, many households begin to treat them as partially pre-allocated—absorbed by systems before they can be used. The psychological impact is subtle but persistent: income growth feels less tangible.

It’s not always obvious where the increase went—only that it didn’t stay.

In some cases, workers respond by adjusting contribution levels or plan selections during open enrollment periods. In others, the structure remains unchanged, and the adjustment happens on the spending side instead.

The Role of Employer Benefit Structures

Employer-sponsored benefits have become a central part of this dynamic.

Health insurance premiums, once relatively stable year-to-year, now show more noticeable increases. Employers often absorb a portion of these costs, but employees still experience rising contributions. High-deductible plans, while offering lower premiums, shift more cost exposure into out-of-pocket spending.

Retirement plans introduce another layer of complexity. Auto-enrollment and auto-escalation features—designed to improve long-term savings participation—gradually increase contribution rates over time. While beneficial from a savings perspective, they reduce immediate take-home pay.

Flexible spending accounts (FSAs), health savings accounts (HSAs), and other pre-tax deductions also affect net income. These are often elected during enrollment periods and remain fixed throughout the year, further shaping paycheck outcomes.

The structure is not inherently negative, but it redistributes how income is experienced: less as direct cash flow, more as allocated resources across multiple categories.

Over time, compensation becomes less about what is received and more about how it is divided before it arrives.

A System-Level Shift in How Income Is Delivered

This pattern reflects a broader structural change in compensation design.

In earlier decades, a larger share of compensation was delivered directly as wages. Benefits existed, but they represented a smaller portion of total compensation. Today, a significant share of employer spending on workers is embedded in non-wage components.

Healthcare, retirement matching, insurance coverage, and compliance-related costs all contribute to total compensation—but they do not appear in take-home pay.

At the same time, regulatory and tax frameworks shape how income flows through payroll systems. Withholding mechanisms are designed to reduce year-end tax imbalances, but they also smooth out income in ways that can obscure changes.

This creates a situation where:

Total compensation may be increasing

Gross wages are rising modestly

But net, usable income grows more slowly

The distinction between earning more and feeling financially ahead becomes more pronounced.

Broader Pattern: Income Growth Is Being Absorbed Before It Reaches Households

This is not limited to a single income bracket or region.

Across urban and suburban areas, similar patterns are emerging. Wage growth, while present, is being partially offset by expanding cost layers embedded within payroll systems.

This aligns with other cost-of-living pressures, including housing, insurance, and utilities, where price increases often occur through structural adjustments rather than visible one-time jumps. It also connects to how short-term credit fills emerging gaps, as explored in When Buy Now, Pay Later Stacks on U.S. Credit Card Debt, where layered financial systems begin to overlap rather than operate separately.

In this context, take-home pay becomes a more accurate reflection of financial capacity than gross income.

But it is also more complex.

The relationship between effort, compensation, and usable income is no longer linear. It is mediated by systems that operate on different timelines and incentives.

Insight: Raises Are Increasingly Distributed Across Systems, Not Just Paychecks

One emerging insight is that raises are no longer experienced as a single, unified increase.

Instead, they are distributed across multiple channels:

A portion increases tax liability

A portion funds higher benefit costs

A portion flows into retirement contributions

And only a portion reaches take-home pay

This distribution is not always visible at the moment it happens. It becomes clearer over time, as workers compare expectations with outcomes.

Insight: The Paycheck Has Become a Compressed Financial Summary

The modern paycheck functions less as a simple payment and more as a compressed financial summary.

It reflects:

Healthcare cost trends

Tax policy adjustments

Employer benefit design

Individual contribution choices

Each pay period becomes a snapshot of multiple systems interacting simultaneously.

Insight: Small Changes, Repeated Over Time, Reshape Financial Perception

No single deduction increase appears dramatic on its own.

A $20 increase in insurance premiums

A 1% rise in retirement contributions

A slight adjustment in withholding

Individually, these changes are manageable. But repeated over multiple cycles, they alter how income is experienced.

Over time, the accumulation matters more than any single adjustment.

Over time, compensation in the U.S. has shifted from direct wages toward layered structures that allocate income across benefits, taxes, and long-term savings before it reaches households.

— Wealth Power Editorial Desk

Income growth is increasingly filtered through layered systems before it reaches households. As deductions expand alongside wages, the paycheck becomes less a measure of earnings and more a reflection of allocation.

Where This Leaves the Modern Paycheck

The idea of a raise remains intact, but its impact has become less direct.

For many workers, the expectation that higher wages will translate into immediate financial flexibility no longer holds in the same way. The systems surrounding income—taxes, benefits, contributions—have become more active participants in shaping what that income ultimately looks like.

This does not necessarily reduce total compensation, but it changes how that compensation is experienced.

It shows up quietly—usually only when someone compares what changed with what actually feels different.

And as these layers continue to evolve, the gap between what is earned and what is available may keep shifting, often without a clear moment when it becomes obvious.