At the start of the year, the raise shows up quietly. A slightly higher salary line on a W-2 job offer update. A few extra dollars per paycheck. On paper, it looks like forward movement — the kind that used to signal stability, even progress.

Within a few months, though, the difference begins to dissolve.

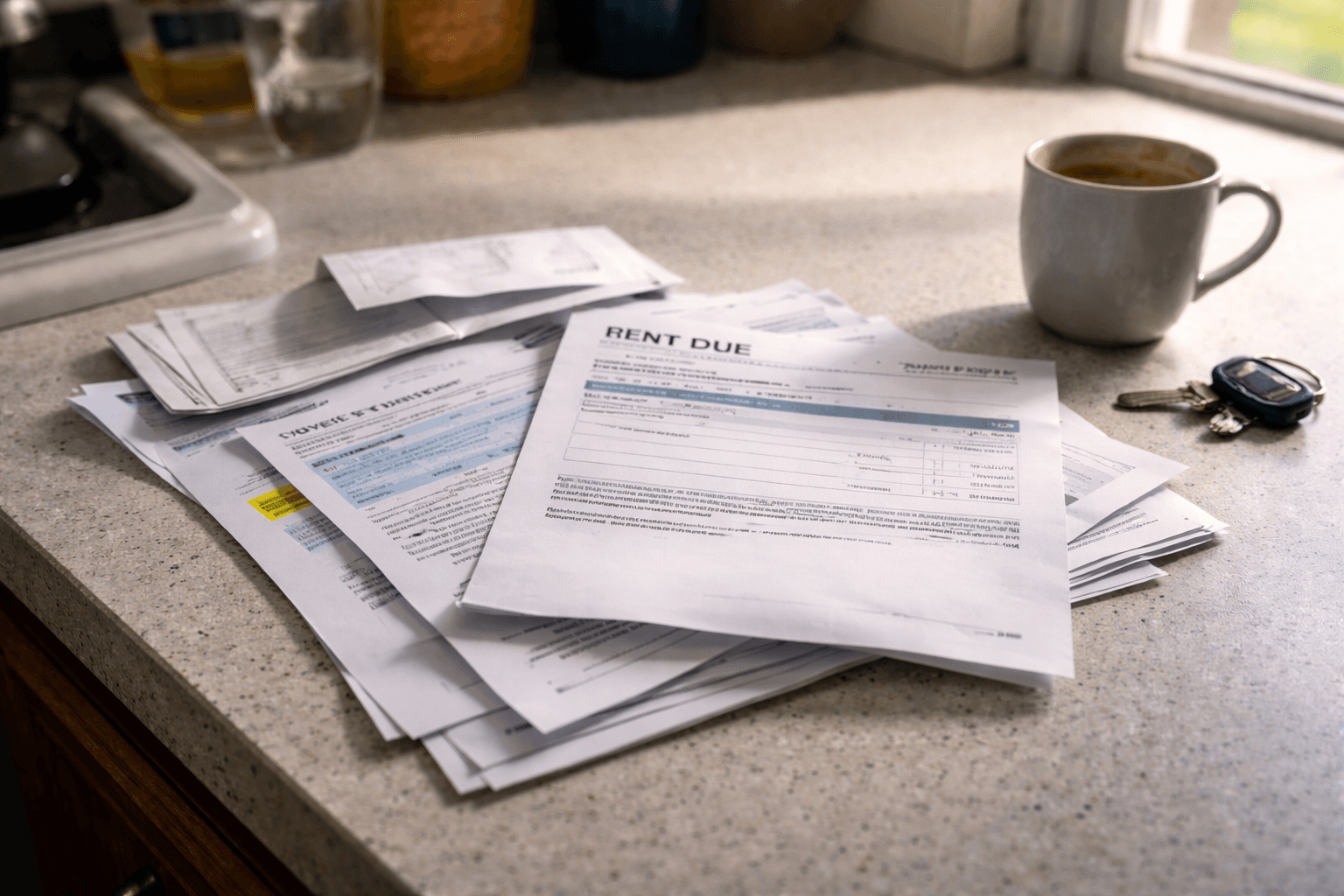

Rent renewals come in higher than expected. Health insurance premiums adjust upward at enrollment. Groceries edge up again, not dramatically, but consistently enough to be noticed at checkout. Utilities fluctuate more than they used to. What initially felt like a raise starts behaving more like a temporary offset.

For many W-2 workers, annual raises are no longer expanding financial capacity. They are simply being absorbed.

That shift is becoming less of a moment — and more of a pattern.

The raise still arrives — but its role looks different now

Annual raises haven’t disappeared. In many sectors, they still follow a predictable cycle: performance reviews, cost-of-living adjustments, merit increases.

The structure remains intact.

What has changed is what those raises actually do.

In previous decades, a raise often created room — a slightly larger buffer after fixed costs. It allowed for incremental changes: saving more, upgrading something, or simply feeling less constrained.

Now, the raise tends to arrive already spoken for.

Before the new income even stabilizes, multiple cost layers adjust alongside it. Rent increases are often timed around lease renewals. Employer-sponsored health insurance premiums shift at the start of the year. Local taxes, insurance premiums, and service costs update on their own schedules — but within roughly the same window.

The result is a compressed financial effect. Income rises once, but expenses rise in multiple places.

Cost increases no longer move in isolation

One of the less visible changes is how synchronized cost pressures have become.

Housing costs don’t just increase — they reset at renewal based on market conditions. Insurance premiums don’t just fluctuate — they recalibrate annually, often with limited transparency. Even subscription services, utilities, and transportation costs now adjust more frequently than they once did.

These changes rarely hit all at once in a single bill. They unfold across a few months, creating a staggered but continuous upward shift in baseline expenses.

A raise, by contrast, is static. It is applied once and remains fixed until the next cycle.

That mismatch creates a slow erosion effect.

A worker might notice that their paycheck is higher, but their remaining balance at the end of each month looks familiar — or tighter. The raise didn’t disappear instantly. It was absorbed gradually, across different categories, each adjusting on its own timeline.

The role of payroll deductions in shrinking visible gains

Another layer sits between gross income and actual take-home pay.

W-2 workers experience raises through payroll systems that automatically adjust for taxes, benefits, and contributions. When income increases, so do certain deductions — sometimes proportionally, sometimes in stepped ways depending on thresholds.

Federal and state taxes take a larger nominal share. Social Security and Medicare contributions increase alongside wages. Employer-sponsored benefits, particularly health insurance, may also claim a larger portion if premiums rise at the same time.

What appears as a 3–5% raise in salary often translates into a smaller percentage increase in net income.

That gap is not always immediately visible, but it becomes clear over a few pay cycles. The expected difference between “before” and “after” feels narrower than anticipated.

In some cases, the net gain aligns closely with — or even trails — the increase in a single major expense, such as rent. Sometimes the difference is small enough that it’s only noticed after a few months of bills stacking up.

Housing resets are outpacing predictable income growth

Housing has become one of the clearest pressure points in this pattern.

Lease renewals now function less like incremental adjustments and more like market resets. Even tenants who remain in place can see significant increases, especially in high-demand urban or suburban areas. This dynamic is increasingly documented in [Lease Renewal Increases Outpacing Wage Growth Across Mid-Sized U.S. Cities], where rent adjustments behave less like inflation and more like repositioning to current market levels.

These increases are often presented within a narrow response window — a new lease rate that must be accepted or declined within days. The timing rarely aligns with income adjustments.

A worker might receive a raise in January, only to face a lease renewal in March that exceeds the entire annual income increase.

The raise was real. But it was overtaken.

Raises follow internal cycles — costs follow markets

There is a structural difference in how income and expenses are determined.

Raises in W-2 roles are typically governed by internal company processes: performance reviews, budget allocations, compensation bands. These systems are designed for stability and predictability. Yet over time, even income growth itself begins to flatten, a shift explored in [Why Career Growth Quietly Slows After Mid-Career], where raises become smaller and less responsive to rising external costs.

Costs, on the other hand, are increasingly tied to external markets.

Housing responds to supply and demand. Insurance premiums adjust based on pooled risk and healthcare pricing trends. Food prices reflect supply chain conditions, transportation costs, and commodity pricing.

These systems operate independently of individual income trajectories.

So while a worker’s raise might follow a steady, annual rhythm, their expenses are influenced by multiple external forces that can shift more quickly — and not always in predictable ways.

This creates a widening gap between how income grows and how costs evolve.

Behavioral adjustments are becoming more subtle

The financial pressure created by this gap doesn’t always lead to immediate, visible changes.

Instead, it often shows up in small behavioral shifts.

Spending decisions become slightly more deliberate. Discretionary purchases are delayed or reconsidered. Subscription services are reviewed more frequently. Savings contributions fluctuate month to month.

These adjustments are rarely dramatic. They are incremental — but consistent.

Over time, they reshape how the raise is experienced.

Rather than enabling new financial movement, the raise becomes part of a balancing act. It helps maintain existing patterns, rather than expand them. A similar pattern appears in [When Income Stops Growing But Expenses Continue], where financial stability becomes more about holding position than moving forward.

The timeline of pressure is getting longer

Another shift is how long these effects last.

Previously, a raise might provide relief for most of the year, with costs catching up gradually. Now, the catch-up period is shorter — and sometimes immediate.

Within three to six months, many workers find that the financial impact of their raise has been fully absorbed.

From that point forward, the remainder of the year feels similar to the one before.

The cycle then resets: anticipation builds toward the next raise, not as an opportunity for advancement, but as a necessary adjustment to keep pace.

Structural layering is replacing single-source pressure

What makes this pattern more persistent is that it’s not driven by a single cost category.

It’s the layering.

Housing, healthcare, food, transportation, and utilities are all moving — sometimes slowly, sometimes in sharper increments. Each one adds a small amount of pressure, but together they create a cumulative effect that outpaces a single annual raise.

This layered structure is harder to counter because it doesn’t present a single point of adjustment.

It also means that even if one category stabilizes temporarily, others may continue rising. Some months feel stable on the surface, but the baseline quietly shifts underneath.

A shift in what “progress” starts to look like

As this pattern becomes more common, the definition of financial progress begins to shift.

A raise no longer guarantees improved financial position. It often signals maintenance — the ability to stay aligned with rising costs rather than move beyond them.

This doesn’t necessarily reflect a failure of income growth.

It reflects a change in the environment around it.

When multiple cost systems adjust simultaneously and continuously, income increases need to do more than they did before just to create the same level of impact.

Raises are still happening, but their function is changing faster than their size.

— Wealth Power Editorial Desk

Frequently Asked Questions

Why does my raise feel smaller than the percentage increase suggests?

Because raises are applied to gross income, while take-home pay reflects taxes, benefits, and deductions. At the same time, multiple expenses may be increasing, reducing the visible impact of the raise.

Are raises actually lower now, or just less effective?

In many cases, raises still fall within typical ranges, but their effectiveness has declined due to faster and broader cost increases across housing, healthcare, and everyday expenses.

Why do expenses seem to rise right after I get a raise?

It’s often a timing overlap. Many cost adjustments — like rent renewals and insurance premiums — occur around the same period as annual raises, making the increases feel directly connected.

Is this pattern affecting most W-2 workers or only certain income levels?

It is being observed across a wide range of middle-income W-2 roles, though the intensity varies depending on location, housing costs, and benefit structures.

The raise still shows up each year, expected and measured.

What changes is harder to see at first — how quickly it blends into everything else already moving.