Table of Contents

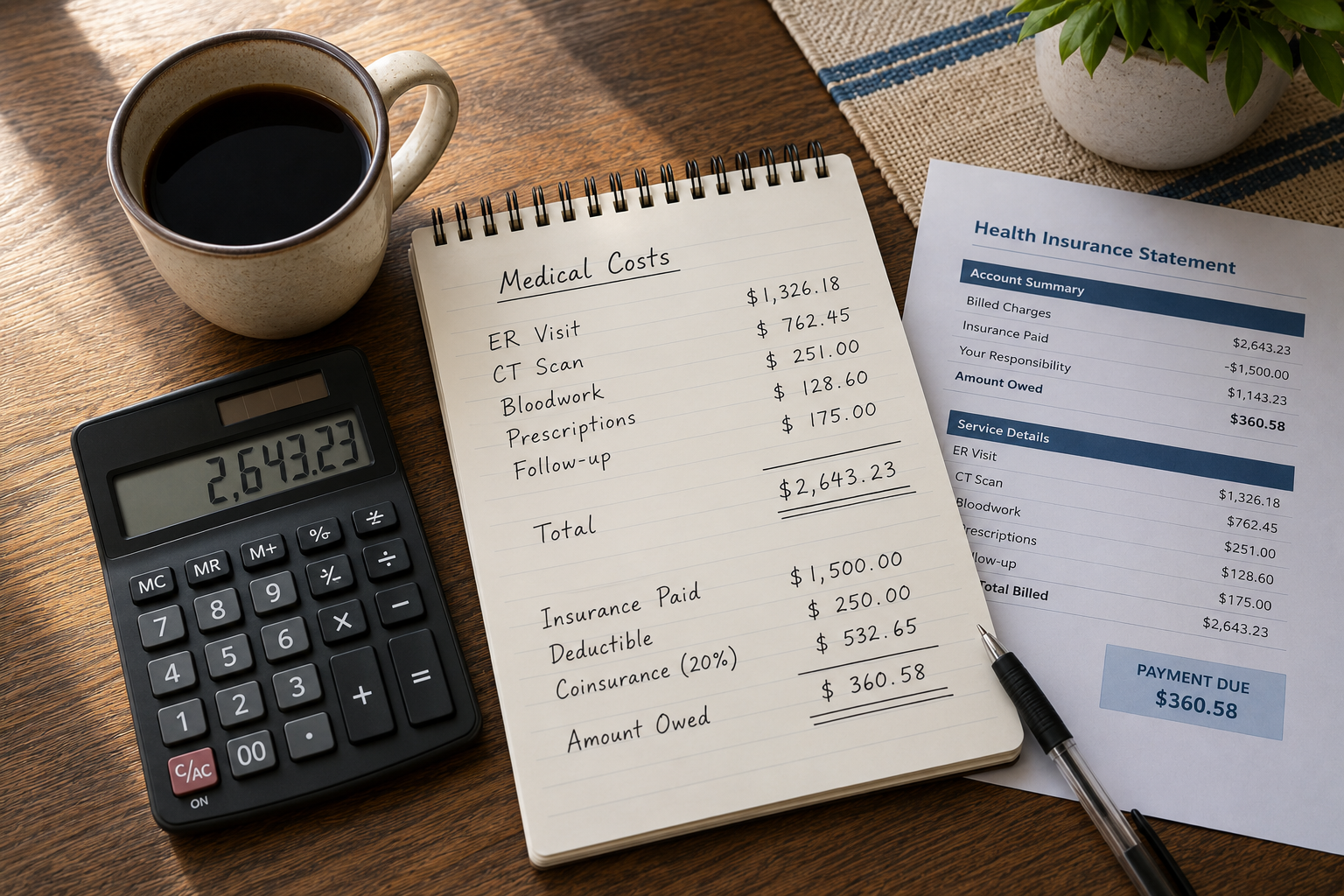

A routine doctor visit that cost $25 last December costs $180 in January. Nothing about the visit changed. The deductible did — it reset to zero on the first of the year, and now every dollar of care gets billed at full price until $2,800 is met. That’s the reality behind high deductible health plan upfront costs: the expense didn’t grow, but the timing of when it lands got a lot less forgiving.

It’s a pattern that rarely makes it into a budget spreadsheet until it’s already reshaped one.

Why the Deductible Reset Hits Harder Than It Looks

The average deductible for workers with single coverage reached $1,886 in 2025, up 17% over the past five years, according to KFF’s Employer Health Benefits Survey. More than a third of covered workers now carry a deductible of $2,000 or more. These aren’t outlier numbers — they’re the median experience for a large share of the U.S. workforce with employer-sponsored coverage.

Consider a hypothetical household: a worker earning $58,000 a year with a $2,800 individual deductible. A 3% raise in January adds roughly $90 to a biweekly paycheck after taxes. That same month, a flu-related urgent care visit and a follow-up prescription land at $310 out of pocket — because none of the deductible has been met yet. The raise that was supposed to create breathing room gets absorbed by a single week of ordinary healthcare use, and the math never quite recovers by February — a version of the same disappearing-raise pattern explored in why a paycheck can feel smaller even when nothing on paper changed.

High Deductible Health Plan Upfront Costs: The Timing Problem Behind the Total

Employers have shifted toward high deductible plans largely because they lower monthly premium costs — a trade that moves financial risk from a fixed, predictable expense to a variable, front-loaded one. From the plan’s perspective, the total annual cost structure often works out close to what a traditional plan would charge. From a household’s perspective, that total gets compressed into the first three or four months of the year, when flu season, routine checkups, and annual physicals cluster naturally.

Income doesn’t follow that same rhythm. Paychecks arrive in steady, even intervals regardless of when medical costs spike. That mismatch — steady income against front-loaded expense — is what actually drives the financial pressure households feel with high deductible health plan upfront costs, more than the total dollar amount ever does.

The same steady-income-against-uneven-expense pattern shows up elsewhere in a household budget too — property tax bills follow an almost identical rhythm, arriving on their own schedule regardless of when a paycheck can actually absorb them.

What Most Households Get Wrong About HSAs

Health Savings Accounts are often positioned as the fix for this exact problem, and they help — but rarely as much as the marketing suggests. Employer HSA contributions typically land in the $500 to $1,000 range annually, a pattern consistent across most employer benefit designs. Against a $2,800 deductible, that contribution offsets roughly a third of the exposure, not the whole thing.

The more useful HSA habit isn’t the employer contribution — it’s treating the account as a dedicated deductible fund rather than a general savings account. Households that redirect a fixed amount from every paycheck into the HSA, timed to arrive before the January reset rather than after the first bill shows up, are the ones who don’t feel the compression the same way. It’s the same discipline that makes a retirement contribution effective: money set aside before it’s needed, rather than found after the fact — and the same discipline that tends to erode once nothing forces a second look, the way retirement contributions quietly do.

Where the Fix Actually Starts

- Front-load your own HSA contributions in November and December, before the deductible resets, rather than spreading contributions evenly across the year. The money needs to be there before January’s expenses arrive, not accumulating alongside them.

- Schedule elective or non-urgent care in the second half of the year, once the deductible is likely already met, rather than in January when every visit costs full price.

- Track deductible progress directly through your insurer’s portal, not by estimating. The gap between “covered” and “applied to deductible” is where most of the confusion — and the delayed care — actually happens.

- Build a separate short-term buffer sized to your deductible, not your full out-of-pocket maximum. Most of the financial pressure hits before the deductible is met, not after.

- Review your HSA contribution rate every time your paycheck changes, the same way a retirement contribution should be reviewed — it’s easy to leave it fixed at a percentage that made sense at a lower deductible or a different salary.

The households that handle high deductible health plan upfront costs well aren’t the ones with the lowest medical bills. They’re the ones who stopped treating January as a surprise and started treating it as a predictable, fundable expense.

Frequently Asked Questions

Q: Should I front-load my HSA contributions or spread them evenly across the year? A: Front-loading before the January reset gives you the most protection, since that’s when deductible-related costs concentrate. If your employer allows adjusting HSA contribution amounts mid-year, increasing contributions in the fourth quarter is one of the most direct ways to prepare.

Q: When does the deductible reset actually take effect? A: For most employer plans, the deductible resets on January 1 regardless of when you enrolled during the year. Some employers use a non-calendar plan year, so it’s worth confirming your specific reset date rather than assuming it’s January.

Q: How does the deductible interact with your out-of-pocket maximum over the course of the year? A: The deductible is the first threshold, but it’s not the last one — coinsurance often still applies after the deductible is met, until the separate out-of-pocket maximum is reached. That second number, not just the deductible, is what determines when costs actually stop climbing for the year.

Q: Is it a myth that switching to a lower-deductible plan always saves money? A: Not necessarily. Lower-deductible plans typically carry higher premiums spread across every paycheck. For someone who rarely hits their deductible, a high deductible plan paired with disciplined HSA contributions can still come out ahead — the decision depends on actual healthcare usage, not just the deductible number alone.

About the Author Craig R. Dunford covers U.S. personal finance, household income behavior, and tax strategy for Wealth Power. His analysis draws on Federal Reserve publications, IRS data, and nearly a decade of tracking financial patterns across American households.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Individual financial situations vary. Readers should consult a qualified financial, tax, or legal professional before making any financial decisions.