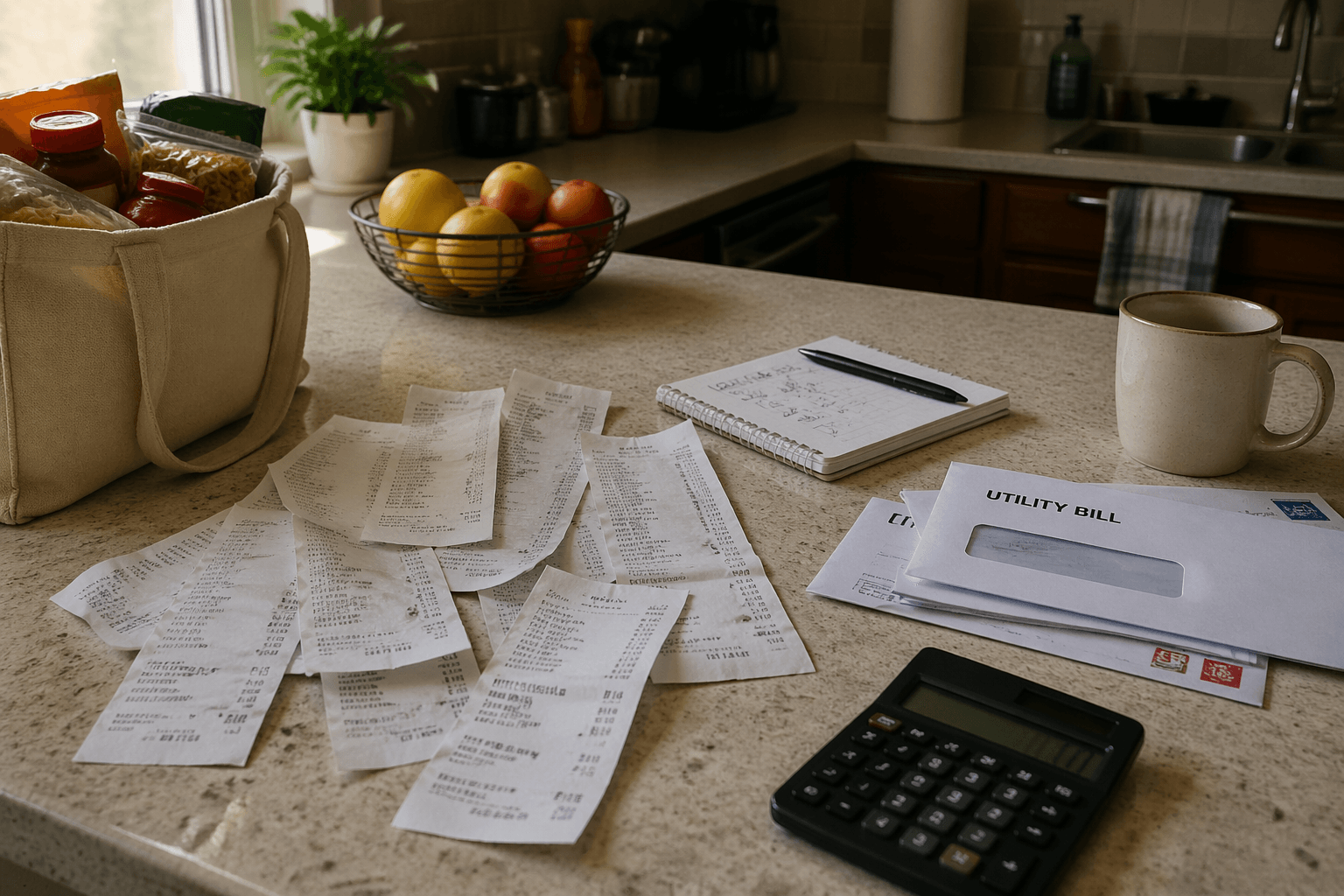

It didn’t feel like a financial problem at first.

The grocery bill was a little higher than usual. The electricity bill ticked up. A couple of subscriptions quietly adjusted their pricing. Nothing dramatic. Nothing that forced an immediate reaction.

That’s how it starts for most households.

Then a few months pass, and something feels off. The same income, the same habits—but less room. Savings slow down. Small decisions start requiring trade-offs.

Not because of one big expense.

Because everything moved at once.

The Real Story Behind Gradual Cost Increases

Most financial pressure today doesn’t come from sudden shocks. It builds through small, distributed increases.

Companies rarely double prices overnight. Instead, they raise them incrementally—$5 here, $10 there—just below the level that triggers immediate behavioral change.

Individually, these increases feel manageable.

Collectively, they reshape your cost structure.

According to U.S. Bureau of Labor Statistics (BLS) Consumer Price Index data, essential categories like food, housing, utilities, and transportation have seen cumulative increases of roughly 15–20% between 2020 and 2024.

That kind of change doesn’t break your budget instantly.

It quietly resets what “normal” costs look like—and most people don’t fully notice until the system stops working the same way.

How Rising Everyday Costs Affect Monthly Budget Stability

The real issue isn’t that one category becomes expensive.

It’s that multiple essential categories rise at the same time.

Consider a realistic U.S. household:

- Net monthly income: $5,400

Then vs Now:

- Rent: $1,550 → $1,850

- Groceries: $650 → $820

- Utilities: $200 → $290

- Insurance: $190 → $270

- Subscriptions & services: $110 → $165

Total increase: ~$695 per month

That’s more than $8,000 per year in additional expenses—without any meaningful lifestyle upgrade.

This is where budgets begin to fail—not because spending became irresponsible, but because baseline costs shifted upward across the board.

Housing is often the biggest driver. In many mid-sized U.S. cities, lease renewals are increasing faster than wage growth, a pattern explored in Lease Renewal Increases Outpacing Wage Growth Across Mid-Sized U.S. Cities.

When your largest expense moves, everything else tightens around it.

Why This Is Happening (System-Level View)

This isn’t random. It’s structural.

There are three underlying forces driving this shift:

1. Broad-Based Inflation

Inflation is no longer concentrated in one sector. It’s spread across essentials—food, energy, housing, insurance—making it less visible but more persistent.

2. Expansion of Recurring Costs

The modern economy has shifted toward subscriptions and recurring billing. What used to be optional or one-time expenses are now fixed monthly obligations.

3. Wage vs. Take-Home Disconnect

Even when wages increase, take-home pay doesn’t always follow at the same pace. Payroll taxes, benefits, and local deductions absorb part of those gains. This is why many workers feel stagnant despite raises, as explained inWage Gains Continue, Yet Take-Home Pay Shrinks as Withholding, Benefits, and Local Taxes Expand.

The result is a slow erosion of real purchasing power—even when income appears stable on paper.

The Delayed Realization Effect

One of the most important dynamics here is timing.

You don’t feel the impact when prices rise.

You feel it when your financial margin disappears.

That usually shows up in subtle ways:

- Savings contributions quietly shrink

- A credit card balance starts carrying over

- Routine purchases require more thought than before

There’s rarely a single breaking point.

Instead, there’s a gradual tightening—a system losing flexibility month by month.

By the time you recognize it, the change has already compounded.

Subtle Financial Shifts That Make It Worse

Beyond visible price increases, a few less obvious shifts amplify the pressure:

Baseline Reset

Your cost of living permanently adjusts upward. What used to be a $4,200 lifestyle becomes $4,800—without intentional change.

Cash Flow Compression

Even if income still covers expenses, the buffer shrinks. This increases vulnerability to unexpected costs.

Invisible Expense Growth

Auto-renewals, bundled services, and incremental upgrades expand categories you rarely review.

Homeowners often experience a similar pattern, where small overlooked costs—maintenance, insurance adjustments, escrow changes—gradually increase total housing expenses, as detailed in Why Hidden Costs Are Increasing Your Monthly Mortgage Expenses.

None of these changes feel urgent individually.

But together, they reshape your entire financial position.

What This Means in Practice

If your budget feels tighter, the solution isn’t guesswork—it’s recalibration.

1. Rebuild Your Budget from Current Reality

Old numbers are outdated. Recalculate your baseline using today’s actual costs.

2. Audit Recurring Expenses Quarterly

Subscriptions, insurance, and utilities now change more frequently than most people track.

3. Separate Inflation from Behavior

Not all spending increases are your fault. Identify what’s price-driven vs. lifestyle-driven.

4. Adjust Income Strategy When Needed

If fixed costs have structurally increased, income needs to respond—not just expenses.

5. Protect Monthly Cash Flow First

Liquidity matters more in a rising-cost environment. Flexibility is what prevents financial stress from turning into debt.

Related Financial Patterns You Should Watch

This pattern connects with other common financial pressures:

- Insurance premiums rising even without claims

- Minimum credit card payments quietly extending debt timelines

- Small tax withholding gaps leading to large year-end balances

Each reflects the same reality:

Financial pressure builds gradually—and becomes visible late.

Conclusion

This didn’t happen overnight.

There was no single expense, no single decision, no obvious turning point.

It was the accumulation of small increases—across rent, food, utilities, and services—layered over time.

And that’s exactly why it’s dangerous.

Because by the time it becomes visible, your financial margin isn’t shrinking anymore—

It’s already gone.

FAQs:

1. Why does my monthly budget feel tighter even without major changes?

Because multiple essential costs have increased at the same time. Even small increases compound and reduce available cash flow.

2. How often should I review my budget now?

Every 3–4 months. Cost structures are shifting more frequently than before.

3. Is this mainly inflation or poor financial management?

In many cases, it’s systemic inflation. The key is identifying whether increases are external or behavioral.

4. When should I focus on increasing income instead of cutting expenses?

When fixed costs like housing, food, and utilities keep rising consistently. At that point, expense reduction alone isn’t enough.

About the Author:

Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.