At forty-three, the house was finally quiet in the middle of a weekday. The mortgage was manageable. The job was steady. Nothing was wrong — and that was exactly the problem.

For millions of American households, financial stability narrows financial room over time in ways that never show up on a bank statement. The paycheck arrives. The bills get paid. And quietly, the margin disappears.

That continuity had been the goal for a long time.

The Numbers Behind the Pattern

This pattern connects directly to why Why Your Tax Bill Keeps Getting Bigger Even When Your Income Stays the Same— a mechanic that quietly accelerates the compression for middle-income households.

According to the Federal Reserve’s 2023 Survey of Consumer Finances, median family income has grown modestly over the past decade — but fixed household expenses including housing, insurance, and debt service have grown faster for middle-income families earning between $50,000 and $100,000 annually.

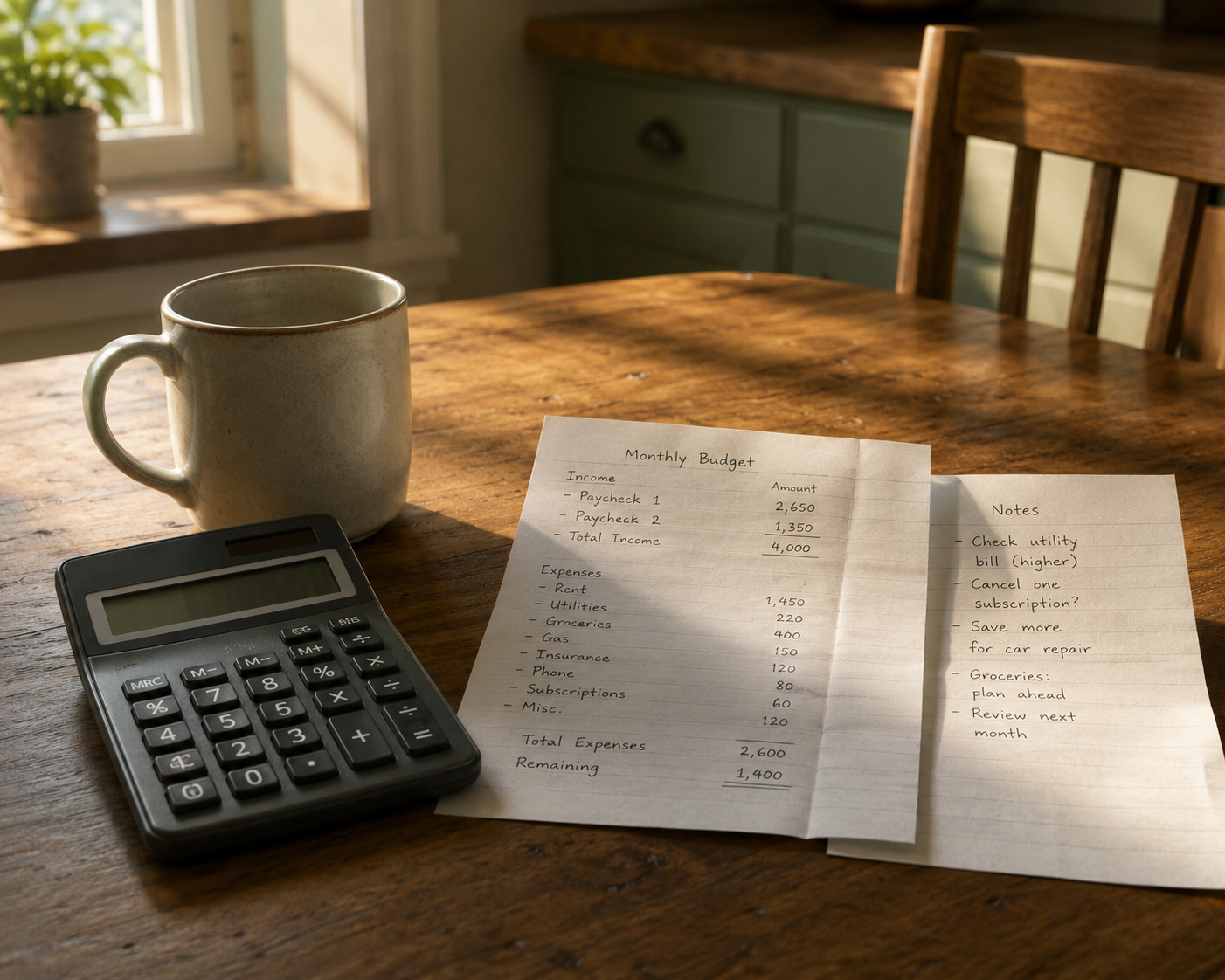

Consider a household in Columbus, Ohio. Combined income of $87,000. Mortgage: $1,650/month. Car payments: $740/month. Health insurance premiums: $610/month. That’s $35,400 in fixed annual costs before groceries, utilities, or childcare. Stable? Yes. Flexible? Not even close.

When Stability Quietly Becomes a Ceiling

This is also why U.S. Bonuses Feel Smaller Than Expected — the gross number looks promising, but fixed obligations and taxes absorb most of it before it changes anything.

In the early years, short-term comfort felt like maturity. A predictable paycheck meant rent was paid without counting days. Groceries went on the list without calculation. Medical bills were inconvenient but not destabilizing. The job absorbed the shocks of life that friends seemed to carry alone. It was common to hear phrases like “at least it’s stable” said with relief, not irony.

Stability became a language everyone understood. It showed up in annual reviews, in holiday conversations with relatives, in the way credit applications were approved without friction. Stability didn’t demand explanation. It spoke for itself.

Over time, that comfort compressed the calendar. Years began to stack without markers. Raises arrived modestly and predictably, just enough to keep pace with bills that also rose quietly. Promotions happened, though they were smaller than expected. Titles changed more than responsibilities. The job grew heavier but not sharper.

Nothing was wrong, exactly.

Short-term comfort has a way of smoothing edges. It removes urgency. It replaces friction with routine. It makes decisions feel unnecessary because tomorrow looks like today, and today is fine. The system works, so there’s no reason to touch it.

By the mid-thirties, the household budget had settled into a shape that resisted disturbance. Fixed costs claimed most of the income before it arrived. Childcare, housing, insurance, commuting, and the small subscriptions that seemed trivial on their own. There was room left, but not flexibility. The margin existed on paper more than in practice.

Comfort created obligations quietly. Each new convenience locked something in place. Each solution solved a problem permanently instead of temporarily. The household ran efficiently, like a well-maintained machine that no one wanted to shut down long enough to examine.

The job’s benefits became structural. Health coverage tied decisions to enrollment periods. Retirement contributions followed preset rules. Time off accumulated but rarely used all at once because coverage was needed. The idea of interruption felt irresponsible, even abstract.

Conversations with peers reflected the same pattern. Everyone spoke about being “fortunate” to have stability, especially when headlines suggested otherwise. Gratitude was sincere. Complaints felt inappropriate. The bar for dissatisfaction rose high enough that it rarely cleared.

When economic shifts happened, the household noticed them mostly through others. Friends relocated. Some changed fields entirely. Others took on unpredictable income in exchange for something they called freedom. Those stories sounded risky, unfinished. Stability insulated against that uncertainty and made it easier to dismiss.

Years later, the consequences of that insulation surfaced slowly.

How Financial Stability Narrows Financial Room Over Time

Income growth flattened, not suddenly, but persistently. The compensation structure rewarded tenure more than leverage. Market changes affected new hires more than existing employees, which felt like protection at first. Over time, it became clear that protection had a ceiling.

Skills aged quietly. Not because they disappeared, but because they became specific to one environment. The work was still competent, still valued internally, but less portable than before. External opportunities required translation that felt harder than expected.

None of this arrived as a crisis. There was no single moment where comfort turned into constraint. It was a sequence of small trade-offs that had already been accepted. Short-term relief had been chosen repeatedly, and each choice made the next one easier.

By the early forties, the household’s financial life looked solid from the outside and narrow from the inside. Cash flow existed, but elasticity didn’t. The idea of disruption carried consequences that had not existed earlier. Health needs were more predictable but more expensive. Family responsibilities extended in both directions. Dependents multiplied, even if some lived elsewhere.

The job continued to function. It paid. It covered. It renewed.

But it no longer expanded.

This is where the story usually gets simplified, but real lives resist clean arcs. There was no regret that could be neatly articulated. Comfort had delivered exactly what it promised. It prevented volatility. It protected continuity. It absorbed shocks.

What it did not do was compound optionality.

It is the same reason U.S. Paychecks Feel Smaller Despite Stable Salaries — the number on the offer letter and the number that actually moves your financial position are rarely the same thing.The margin does not disappear overnight. It compresses slowly, decision by decision, until the household that once felt financially secure realizes it has no room left to move.

The Hidden Trade-Off Most Households Never See

Short-term comfort tends to borrow from the future in ways that don’t show up on statements. It pulls forward ease and pushes back growth. It trades uncertainty now for limitation later, but the exchange rate is invisible until much later.

In many households, this realization arrives indirectly. Through a job posting that looks unfamiliar. Through a salary range that hasn’t moved as much as expected. Through the sense that changing anything would require moving many things at once, not one.

The financial system rewards predictability. Lenders like it. Employers like it. Even families like it, because it reduces anxiety. Predictability has value. The issue is not that it exists, but that it accumulates.

Comfort is sticky. Once installed, it resists removal.

In quieter moments, often late at night or early in the morning, the thought surfaces without drama. Not panic. Not urgency. Just awareness. The household is stable, but not mobile. Secure, but not flexible. Covered, but not expansive.

That awareness doesn’t demand action. It doesn’t announce itself loudly. It sits alongside the rest of life, another line item that doesn’t have a clear category.

The dining table still serves as a desk some days. The window still lets in the same light. The neighborhood still looks unchanged. Stability continues to do its job.

What happens next is not obvious. It rarely is. Comfort does not collapse on its own. It also doesn’t transform.

It simply holds.

And keeps holding.

What This Means in Practice

Track your fixed cost ratio. Divide your total monthly fixed expenses by your gross monthly income. If that number exceeds 50%, your financial room is already compressed.

Treat lifestyle upgrades as permanent commitments. Every subscription, lease, or recurring payment locks in a future obligation.

Stability is not the same as security. A household with $87,000 income and $35,000 fixed costs

has less real security than one earning $65,000 with $18,000 fixed costs.Renegotiate fixed costs every 24 months. Insurance premiums and subscriptions rarely self-correct.

Q: At what point does financial stability become a trap? A: When fixed monthly obligations exceed 45–50% of gross income, stability starts working against flexibility.

Q: When should a household start worrying? A: Mid-thirties — when fixed costs have accumulated across a decade of reasonable decisions.

Q: How does U.S. tax structure make this worse? A: A $5,000 raise at $85,000 income may net only $3,200 after taxes — while fixed costs rise by the full amount.

About the Author. Craig R. Dunford covers U.S. personal finance, household income behavior, and tax strategy for Wealth Power.

Disclaimer: This article is for. informational and educational purposes only and does not constitute financial, tax, or legal advice.