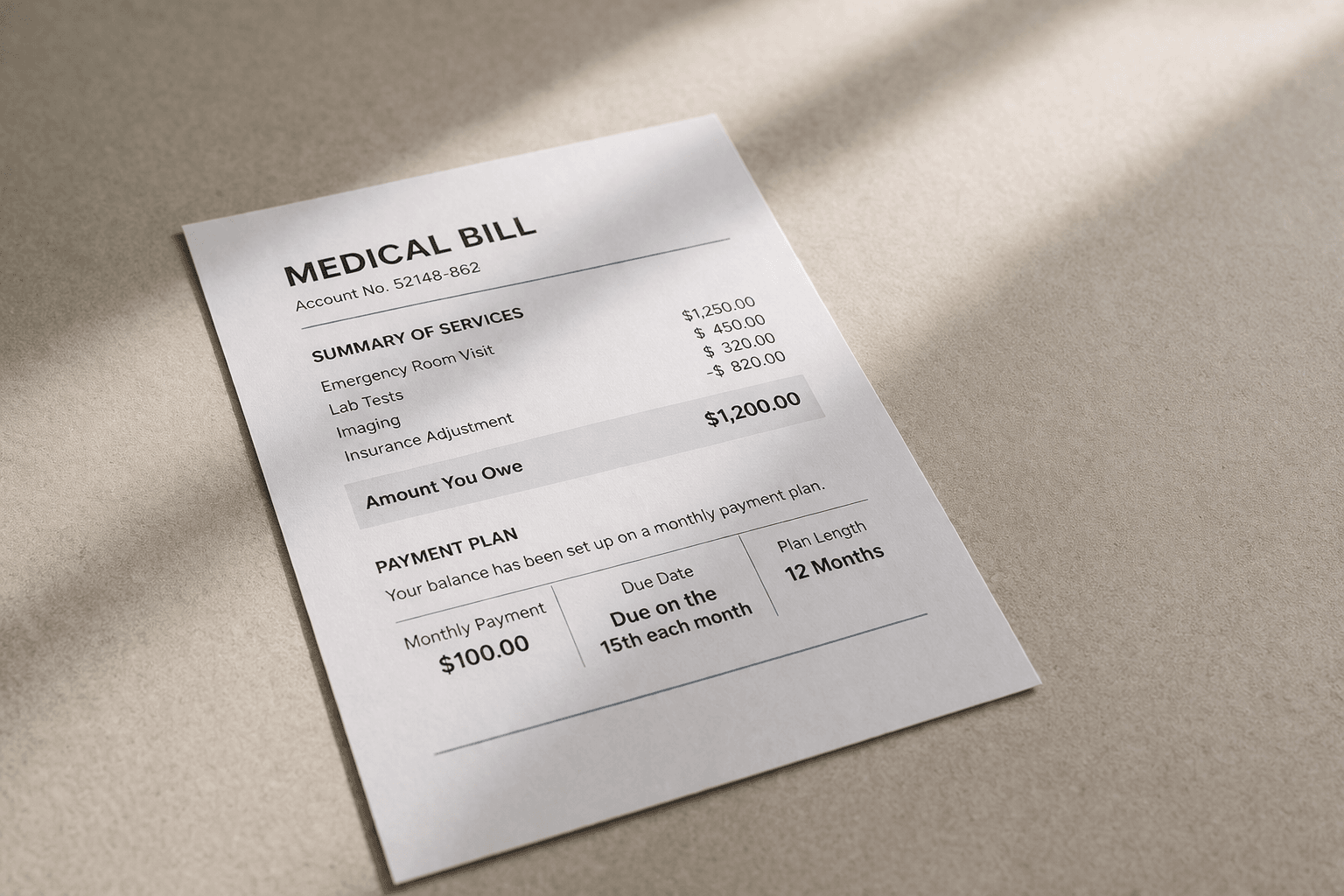

A $1,200 medical bill gets split into monthly payments. The hospital portal shows a manageable plan—$100 a month, no immediate interest.

But the credit card statement still arrives with a $3,400 balance. The minimum payment is due, unchanged. And now, both obligations begin drawing from the same paycheck.

For many U.S. households, this is where financial pressure doesn’t spike—it layers. One payment plan sits beside another, each manageable on its own, but harder to absorb together.

Medical payment plans have become a common way to handle out-of-pocket healthcare costs in the U.S. After insurance, remaining balances—often tied to deductibles, co-insurance, or uncovered services—are frequently converted into structured monthly payments.

On paper, these plans can feel contained. They often don’t carry the same visible interest as credit cards, and they are usually presented as a short-term arrangement.

But they rarely exist in isolation.

Most households entering a medical payment plan are already managing ongoing financial commitments—rent or mortgage payments, auto loans, insurance premiums, and, in many cases, existing credit card balances.

The medical plan doesn’t replace these obligations. It joins them.

This is where the layering begins to take shape.

A $100 monthly medical payment may seem manageable against a steady income. But when added to a $120 credit card minimum, a $300 auto loan, and rising insurance costs, the structure of monthly obligations starts to tighten.

This often shows up not as an immediate strain, but as a reduction in flexibility.

There’s less room to absorb unexpected expenses. Less space between income and obligations. And less ability to shift spending across the month.

Over time, smaller fixed payment structures can begin to function like long-term financial commitments.

— Wealth Power Editorial Desk

The interaction between medical plans and credit cards introduces another layer of complexity.

Medical providers typically expect consistent, fixed payments. Missing a payment can lead to account escalation or collections. These plans don’t usually allow for the same flexibility as credit cards, where minimum payments can be adjusted relative to balance.

As a result, medical payments often take priority in the monthly sequence.

This can shift how credit card balances are managed.

Instead of making larger payments to reduce interest, households may lean more heavily on minimum payments to preserve cash flow for fixed obligations like medical plans.

Over time, this changes how credit card debt behaves.

Balances that might have declined more quickly begin to stabilize or grow, as interest continues to accumulate in the background.

There is also a timing effect that becomes visible over the course of a billing cycle.

Medical payments may be scheduled mid-month, while credit card due dates fall at the beginning or end of the cycle. When combined with rent, utilities, and insurance premiums, these staggered dates can compress available cash flow into specific windows.

A household might technically cover all obligations across the month, but still experience short-term gaps where expenses cluster together.

This often means credit cards begin to absorb those gaps.

A utility bill or grocery purchase that would have been covered by available cash instead moves onto revolving credit—not because of increased spending, but because of how payments are distributed.

A similar pattern appears when other short-term financing systems begin to overlap. As seen in When Buy Now, Pay Later Stacks on U.S. Credit Card Debt, installment-based payments can quietly layer onto existing balances, further dividing how monthly income is allocated.

Another dynamic emerges in how these obligations are perceived.

Medical debt is often viewed as temporary—a bill tied to a specific event. Credit card debt, by contrast, is ongoing and revolving.

But when a medical payment plan extends over 12 or 18 months, that distinction begins to blur.

The payment becomes part of the regular monthly structure, similar to a loan or subscription.

For many households, this reflects how temporary expenses can transition into ongoing financial commitments once they are structured into installments.

At the same time, different forms of debt management can interact in less visible ways. As explored in Why 0% APR Balance Transfers Can Hide Real U.S. Debt Pressure, shifting balances across accounts may reduce immediate interest but does not remove the underlying obligation from the monthly system.

There is also a cumulative effect across time.

A single medical event may lead to one payment plan. But new expenses can arise before the previous plan ends—follow-up visits, prescriptions, or additional procedures.

This creates overlapping timelines.

Instead of a single, contained obligation, households may find themselves managing multiple medical payments alongside existing credit card balances.

Each plan has its own schedule, its own due date, and its own impact on monthly cash flow.

Another layer begins to appear when income changes do not translate directly into increased flexibility.

A household may experience a raise or take on additional work, but the resulting income can be partially offset by tax adjustments. As outlined in Why Side Income Can Increase U.S. Tax Burden Over Time, the usable portion of that income may not expand as much as expected.

This often means that even as earnings rise, the capacity to absorb overlapping payments remains limited.

Over longer periods, the structure itself becomes the defining factor.

It is not just the size of each payment, but how many separate commitments exist at once. A $90 medical payment, a $110 credit card minimum, and a $250 auto loan may all seem manageable independently.

Together, they form a system that steadily draws from the same income.

This often means financial pressure is no longer tied to a single bill, but to the accumulation of multiple smaller ones.

What makes this structure difficult to identify is that it rarely presents as a clear financial problem.

There’s no single bill that appears unmanageable. No immediate spike in total debt.

Instead, the pressure distributes itself across time—through fixed payments, staggered due dates, and overlapping obligations.

For many U.S. households, this reflects a broader pattern in how financial strain develops. It becomes less about large, one-time expenses and more about how multiple smaller commitments interact within the same income cycle.

Over time, the distinction between manageable payments and cumulative obligation becomes more visible.

A medical plan may feel temporary at the start. A credit card balance may feel flexible. But together, they form a structure that draws consistently from the same pool of income.

And as that structure settles into the monthly cycle, the experience of debt shifts—from something episodic to something continuous, shaped by how payments overlap rather than how they begin.

In many households, this structure doesn’t feel restrictive at first. Payments are scheduled, accounts are current, and nothing appears immediately out of control. The system continues to function, even as more obligations are quietly added.

But over time, the pattern becomes easier to notice in smaller moments.

A paycheck arrives, and most of it is already accounted for. A portion moves toward fixed obligations—medical plans, credit card minimums, auto payments—while the remaining balance begins to narrow more quickly than expected. The margin between income and expenses becomes thinner, not because of a single large cost, but because of how many separate payments now exist at once.

This often leads to a subtle shift in how financial decisions are experienced.

Instead of evaluating one expense at a time, households begin navigating a sequence of commitments that repeat every month. Each obligation has its own due date, its own priority, and its own impact on available cash flow.

For many U.S. households, this reflects how financial pressure becomes embedded within the structure itself. It is not always driven by rising debt alone, but by how multiple payment systems—medical, credit, and everyday expenses—interact within the same income cycle.

Over longer periods, this interaction can make the financial system feel stable on the surface while gradually becoming more constrained underneath.

And as these overlapping timelines continue, the challenge is no longer tied to a single bill or balance, but to how the entire structure continues to draw from the same income, month after month.

Leave a Reply