By Craig R. Dunford, Wealth Power

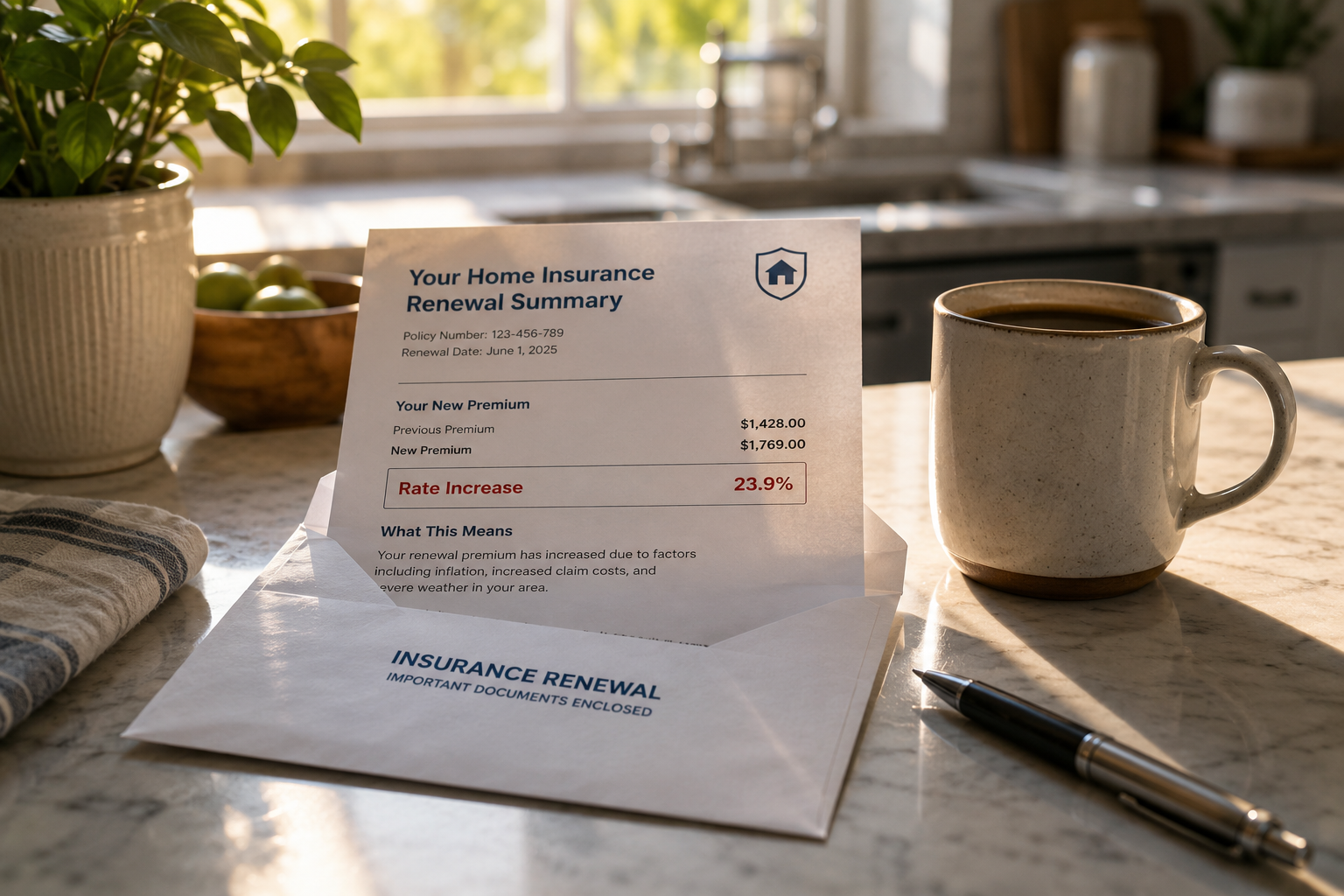

A renewal notice for $3,200 a year on a policy that cost $1,640 just five years ago is not a typo. It is the new normal for a growing share of American homeowners, and the number rarely moves back in the other direction.

Homeowners insurance premiums have risen for five straight years nationally, and for most U.S. households, the annual renewal has quietly become one of the least predictable line items in the entire housing budget.

The math behind that statement is not abstract. According to LendingTree’s analysis of insurer rate filings, U.S. home insurance rates climbed a cumulative 46.8% nationally between 2020 and 2025, and increases have touched every single state in the country. This isn’t a regional anomaly tied to one bad hurricane season. It’s a structural shift in how insurers price risk in America.

Consider a hypothetical household that illustrates the pattern well: a married couple in Lakewood, Colorado, with a combined income of $118,000, a $310,000 mortgage balance, and a home purchased in 2019. Their homeowners premium ran roughly $1,640 a year at closing. By 2025, a renewal in that range would plausibly cross $3,200, in line with Colorado’s reported increases. Nothing about the house would need to change for that to happen. No claims filed. The roof is the same roof. What changes is the pricing model surrounding the home — and that model doesn’t reset just because the property hasn’t.

That same household, like most American families carrying a mortgage, is also navigating other costs that quietly compound on top of the loan itself — a dynamic worth understanding on its own terms, since the hidden charges that inflate a mortgage payment beyond principal and interest rarely get explained clearly at closing.

Why Homeowners Insurance Premiums Don’t Move in Reverse

Homeowners insurance premiums aren’t anchored to a fixed agreement the way a mortgage is. A 30-year fixed mortgage locks a rate for three decades. A homeowners policy gets re-priced every single year, based on a rolling assessment of risk that has almost nothing to do with whether your specific house behaved itself.

That distinction matters more than most homeowners realize. Mortgage payments feel permanent because they are. Insurance premiums feel arbitrary because, in a sense, they are recalculated from scratch annually — against a backdrop that keeps getting more expensive to underwrite. “It’s a frustrating asymmetry: the one housing cost homeowners expect to stabilize over time is often the one that doesn’t — and homeowners insurance premiums are the clearest example of that pattern.

Insurify’s 2026 forecast reports that U.S. home insurance premiums have risen for a fifth straight year in 2026, with insurers contending with losses from extreme weather and elevated rebuilding costs. Since 2021, premiums have climbed 46%, roughly three times the rate of inflation, according to the same data. That gap — premiums outpacing inflation by a factor of three — is the detail most coverage skips past. It means insurance isn’t just getting more expensive in absolute terms. It’s eating a growing share of household budgets relative to everything else.

There’s an emotional layer to this that rarely gets acknowledged. Homeowners do the responsible thing — they pay on time, avoid claims, maintain the property — and still watch the bill climb. It makes sense that this feels unfair. It also doesn’t change how the pricing model works.

The Real Driver Behind Rising Homeowners Insurance Premiums

The popular explanation is “climate change,” and that’s directionally true but incomplete. The more precise driver is what it now costs to physically rebuild a home after a covered loss.

According to InsuredBetter, lumber, asphalt, and roofing materials remain significantly more expensive than they were before 2020, even as general inflation has cooled. Insurers price policies against replacement cost — what it would take to rebuild the structure today, not what you paid for it. When construction costs rise, the dwelling coverage limit on your policy has to rise with it, and the premium follows.

…your homeowners insurance premium can increase… even if your insurer has never once raised your coverage limit. NerdWallet’s 2026 survey found that 21% of Americans with homeowners insurance cited severe weather or natural disasters as a direct factor behind rate increases in their area, but materials and labor costs touch nearly every policy in the country, regardless of region.

There’s a second layer here that rarely gets discussed: insurers don’t just react to your house. They react to the entire reinsurance market — the insurance that insurance companies buy to protect themselves against catastrophic losses. When reinsurance gets more expensive after a bad year of claims nationally, that cost flows downstream into every renewal notice, including yours, even if your specific ZIP code had a quiet year.

This mechanism explains something that confuses a lot of homeowners: why a neighbor two states away filing a hurricane claim can somehow show up in your premium a year later. The risk pool is national and reinsurance-driven, not local and claims-driven, even though it doesn’t feel that way from the renewal notice alone. It’s also worth knowing that pricing doesn’t always wait for the annual renewal — what actually triggers a rate change in the middle of an active policy is a separate question with its own set of answers, and one that catches a lot of homeowners off guard.

Regional Risk Has Created a Two-Tier Insurance Market

Geography now explains a wider gap in homeowners insurance premiums than almost any other factor. According to LendingTree’s state-by-state data, Oklahoma homeowners pay an average of $5,298 a year, more than double the national average, while Hawaii homeowners pay roughly $801 — a gap driven almost entirely by exposure to severe convective storms, hail, hurricanes, and wildfire.

The states getting hit hardest aren’t always the ones you’d expect. Insurify’s data, reported by The Hill, shows that severe convective storms — the kind that produce tornadoes and softball-sized hail — caused more than $52 billion in insured losses in 2025 alone, the third-highest total on record. That activity has pushed double-digit rate increases through Minnesota, Colorado, Iowa, Nebraska, Oklahoma, and South Carolina — states with no coastline and no wildfire exposure, simply absorbing the cost of an increasingly volatile Midwest storm pattern.

Meanwhile, a handful of states — Hawaii, Massachusetts, Maine, Louisiana, and Rhode Island — are projected by Insurify to see rates fall slightly in 2026. That’s the detail that complicates the “insurance only goes up” narrative. It doesn’t always go up everywhere at once — but where it falls, it tends to fall by a percent or two, while in high-risk states it climbs in double digits. The asymmetry between the two is what defines this market right now.

What This Means for the Cost of Owning a Home Long After the Mortgage Is Set

Here’s the part that catches long-term homeowners off guard: the mortgage is the one cost you can lock down. Insurance is the one you can’t.

A homeowner who refinanced into a 3% rate in 2021 has a fixed, predictable mortgage payment for the life of the loan. That same homeowner’s premium on their homeowners insurance has had no such ceiling. It’s increasingly common for the insurance line of a monthly housing budget to grow faster than the mortgage payment itself over a decade of ownership.

A 2026 survey from The Zebra found that 47% of homeowners say they would struggle to pay their mortgage if their insurance premium rose further, and 74% say insurance now makes up a significant portion of their total housing budget. That’s not a niche concern. That’s a description of how home insurance has repositioned itself within the household balance sheet over the past five years.

Research cited by industry outlets has linked rising premiums to a measurable effect on home values: a 10% rise in homeowners insurance costs has been associated with roughly a 4-5% decline in home prices in affected markets, particularly in high-risk states where coverage has become harder to obtain at any price. The relationship works both ways — rising premiums don’t just strain current owners, they start to suppress what buyers are willing to pay.

There’s a parallel worth drawing here to how other fixed-looking obligations quietly expand over time. A household carrying credit card debt sees something structurally similar play out, just on a faster timeline — how a minimum payment can stretch a balance into a decade-long burden follows the same logic of a cost that looks manageable in any single month but compounds into something much larger over years.

What This Means in Practice

- Shop your policy every renewal, not just at purchase. Rate filings vary by carrier and region, and getting quotes from smaller regional insurers, not just national brands, is one of the more effective ways homeowners can offset rising costs. A policy that was competitively priced three years ago may no longer be.

- Raise your deductible deliberately, not by default. NerdWallet’s rate analysis found that moving a deductible from $1,000 to $2,500 saves homeowners roughly 9% a year on average — but that move only makes sense if you have the cash on hand to actually cover that deductible if a claim hits.

- Check your flood coverage status even outside official flood zones. Updated FEMA flood maps are pulling more properties into designated flood zones than before, and flood premiums for newly added properties are climbing more than 10% a year — a coverage gap that catches buyers who assumed their area was never at risk.

- Don’t let a clean claims history make you assume your rate is locked. Your premium moves with regional and national risk data, not just your own claims history. A clean record can slow the rate of increase; it doesn’t stop it.

- Treat insurance as a variable cost, not a fixed one, when running long-term affordability numbers. If you’re stress-testing what a home costs you in year ten, model insurance at a higher figure than your current premium — not the same number you’re paying today.

The mortgage was never the whole story of what a home costs. Insurance has become the part of that story that keeps writing new chapters every year, regardless of what the house itself is doing.

If there’s one number worth tracking annually, it’s not your homeowners insurance premium in isolation — it’s your premium as a share of your total housing payment. Rates increased 6% nationally in 2025 alone, according to LendingTree, and households absorbing that increase without adjusting their coverage strategy are the ones most likely to feel squeezed when the next bad storm season hits.

FAQ

Q: Should I switch insurance carriers every year to chase the lowest premium? A: Not automatically, but you should requote every renewal. Carriers reprice risk differently and at different times, so the cheapest option when you bought the house is rarely the cheapest five years later. Compare at least three quotes with identical coverage limits and deductibles before switching, since a lower premium with a lower coverage limit isn’t actually a better deal.

Q: When does it actually make sense to raise my deductible? A: When you have enough liquid savings to comfortably cover the higher deductible amount without financial strain if you need to file a claim. If raising your deductible from $1,000 to $2,500 would leave you unable to pay that $2,500 out of pocket, the savings aren’t worth the risk.

Q: Why don’t homeowners insurance premiums stay the same if I haven’t filed a claim? A :For many carriers, pricing is based on pooled regional and national risk data, not solely individual claims history. Rebuilding costs, reinsurance pricing, and regional weather patterns can factor into a renewal even when a homeowner’s personal record is spotless — though exact underwriting methods vary by company and state.

Q: Is it a myth that home insurance only goes up? A: Mostly true as a national pattern, but not universal. A small number of states are projected to see modest rate decreases in a given year. The more reliable pattern is asymmetry: increases tend to be larger and more frequent than decreases, especially in high-risk states.

About the Author Craig R. Dunford covers U.S. personal finance, household income behavior, and tax strategy for Wealth Power. His analysis draws on Federal Reserve publications, IRS data, and nearly a decade of tracking financial patterns across American households.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Individual financial situations vary. Readers should consult a qualified financial, tax, or legal professional before making any financial decisions.