In January, your budget felt stable. Bills were predictable, savings were on track, and nothing seemed out of place. By mid-year, something changed—but not in a way you could clearly point to. Your checking account started running lower before payday. Credit card balances didn’t fully clear like they used to.

That’s when it clicks: a cost of living increase in monthly expenses—unnoticed at first—has already reshaped your finances.

The Slow Shift That Breaks Stable Budgets

Most financial strain doesn’t come from one large expense. It builds through small increases across essential categories.

A grocery trip that used to cost around $120 now quietly hits $150. Insurance renewals come in higher than expected. Utility bills edge up with seasonal and rate changes. Subscriptions increase by a few dollars at a time. None of these feel urgent on their own.

According to the U.S. Bureau of Labor Statistics, essential categories like food at home and housing have seen persistent price increases in recent years, with food prices alone rising notably year-over-year in multiple periods. For many households, these increases outpace how quickly income adjusts.

The result isn’t immediate stress. It’s delayed pressure—and by the time you feel it, your baseline cost has already shifted.

Cost of Living Increase Monthly Expenses Unnoticed: Why It Happens

The system is built for low-friction spending.

Most expenses today are automated. Rent, insurance, utilities, streaming services—everything renews without requiring active decisions. When prices increase, they rarely interrupt your routine.

At the same time, income doesn’t adjust in real time. Even when raises happen, they’re often partially offset by taxes, benefit deductions, or simply lag behind rising costs. This becomes even more visible later in your career, where income growth slows while fixed costs continue rising—something explored in Why a Late-Career Salary Plateau Can’t Keep Up With Rising Insurance, Tax, and Healthcare Costs.

There’s also a behavioral gap. People anchor to an older version of their budget. If you’ve been spending around $3,500 a month, you don’t immediately register when that quietly becomes closer to $3,900.

That gap—between what you think you spend and what you actually spend—is where financial pressure builds.

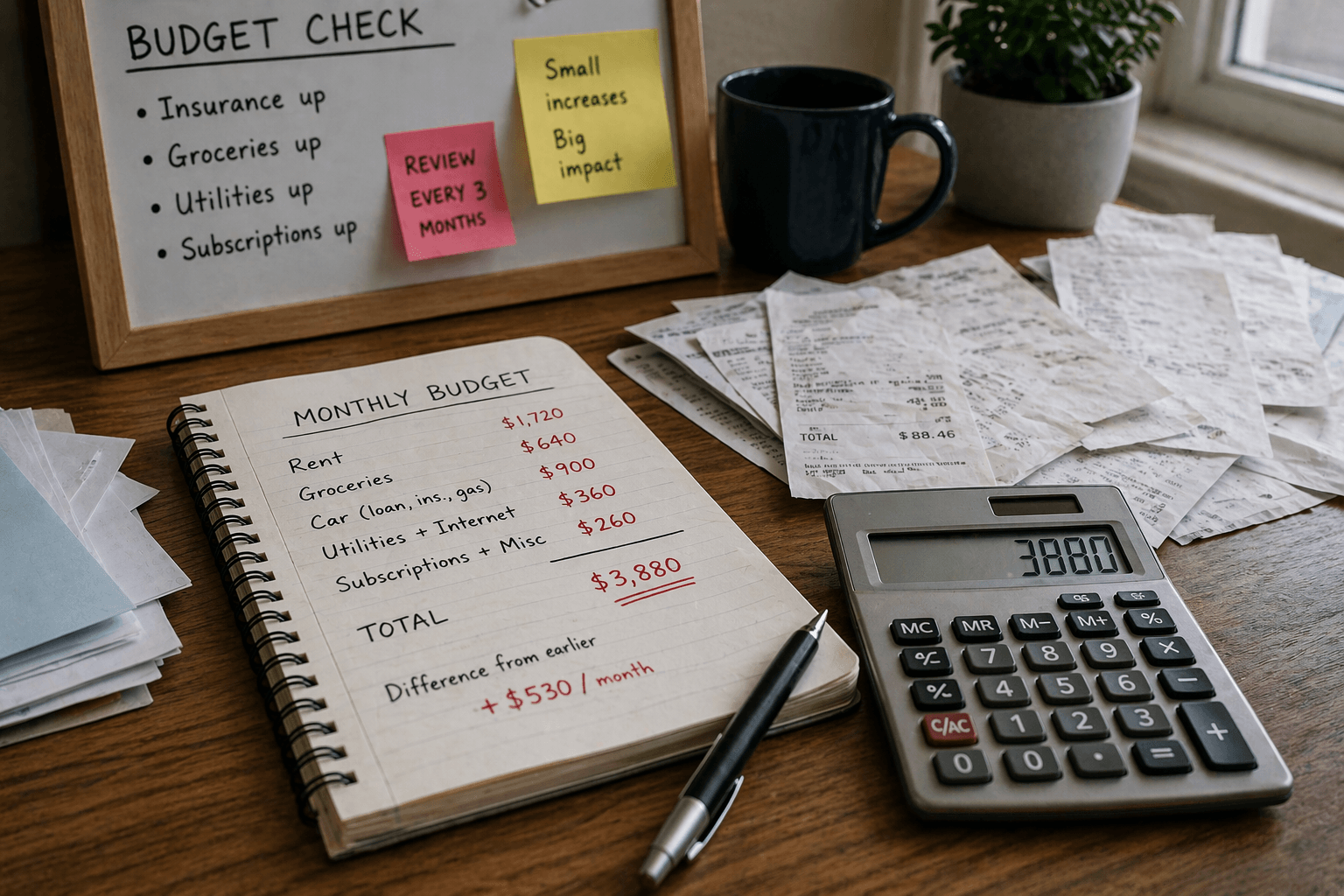

A Real Household Example: Where the Money Actually Went

Consider a dual-income household in Ohio earning a combined $92,000 annually.

At the start of the year, their monthly budget looked like this:

- Rent: $1,600

- Groceries: $500

- Car expenses (loan + insurance + gas): $750

- Utilities + internet: $300

- Subscriptions + misc: $200

Total: ~$3,350

Six months later, without any lifestyle upgrades:

- Rent renewal: $1,720

- Groceries: $640

- Car loan: $400 (unchanged)

- Car insurance: $240 → $330

- Gas: $110 → $170

- Utilities (seasonal + rate hikes): $300 → $360

- Subscriptions creep: $200 → $260

New total: ~$3,880

That’s a $530 monthly increase—over $6,300 annually—without a single “big decision.”

In many cases, this doesn’t immediately trigger a budget reset. Households often absorb the gap quietly at first—usually by reducing savings or carrying small credit balances that gradually grow.

Why This Matters More Than It Seems

This kind of gradual cost expansion affects more than just your monthly cash flow.

First, it compresses savings without visibility. A household saving $500 per month may see that drop toward zero without ever making a conscious decision to cut back—effectively reducing their savings rate from around 15% to near nothing.

Second, it increases reliance on short-term credit. Federal Reserve data has shown elevated credit card balances in recent periods, with a meaningful portion tied to everyday expenses rather than discretionary spending.

Third, it distorts financial planning. Retirement contributions, emergency funds, and tax strategies are all built on assumptions. If your actual expenses have shifted, those plans quietly become misaligned.

Over time, this compounding effect becomes more structural—similar to how the cost of expanding a stable financial life gradually increases fixed obligations without a clear decision point.

The Structural Layer Most People Miss

This isn’t just about personal budgeting discipline.

Many essential costs—housing, insurance, healthcare—are structurally rising and often reset on annual cycles. These increases aren’t always transparent, and they rarely happen all at once. In housing specifically, this shows up through the quiet compounding of property taxes and insurance, which can significantly alter long-term affordability.

At the same time, the definition of “basic expenses” has expanded. Multiple subscriptions, higher-tier data plans, delivery services—these are now embedded into normal monthly spending in a way they weren’t a decade ago.

So the system is doing two things simultaneously:

- Raising prices

- Expanding what counts as a standard expense

That combination makes cost creep harder to notice—and faster to accumulate than most people expect.

What this means in practice

- Recalculate your real monthly baseline every 90 days

Use actual bank and credit card data—not estimates—to identify your current fixed cost level. - Review renewals before they hit

Insurance, rent, and subscriptions should be evaluated ahead of renewal dates, when you still have options. - Separate inflation from behavior

Identify which increases are market-driven versus choice-driven. You can only directly control one of them. - Adjust financial targets in real time

If your expenses rise by $500 per month, your emergency fund and savings targets should increase accordingly. - Watch early signals, not late outcomes

A shrinking checking account buffer is often the first sign. Rising credit card balances come later.

Related patterns worth watching

You’ll see similar delayed-impact patterns in how minimum credit card payments extend repayment timelines, how insurance premium resets affect annual budgets, and how tax withholding gaps create unexpected year-end balances.

Each follows the same principle: small, system-driven changes that compound before they become obvious.

Conclusion

The most impactful financial changes rarely feel dramatic when they happen. They build quietly, across categories, without forcing immediate attention.

A cost of living increase in monthly expenses—unnoticed at first—doesn’t break your budget overnight. It shifts it gradually, until the numbers stop working.

By the time you notice, the structure has already changed. What matters then is how quickly—and how realistically—you adjust.

FAQs

Why do small increases feel so hard to track?

Because they’re spread across multiple categories and often tied to automatic payments. There’s no single moment that forces you to notice.

How often should I reset my budget baseline?

Every 3–4 months. Waiting longer increases the gap between perception and reality.

Is this mainly inflation or lifestyle creep?

It’s both. Inflation raises prices, while modern spending patterns increase the number of recurring costs.

What’s the earliest warning sign?

Your monthly cash buffer starts shrinking even when your income hasn’t changed.

About the Author: Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.