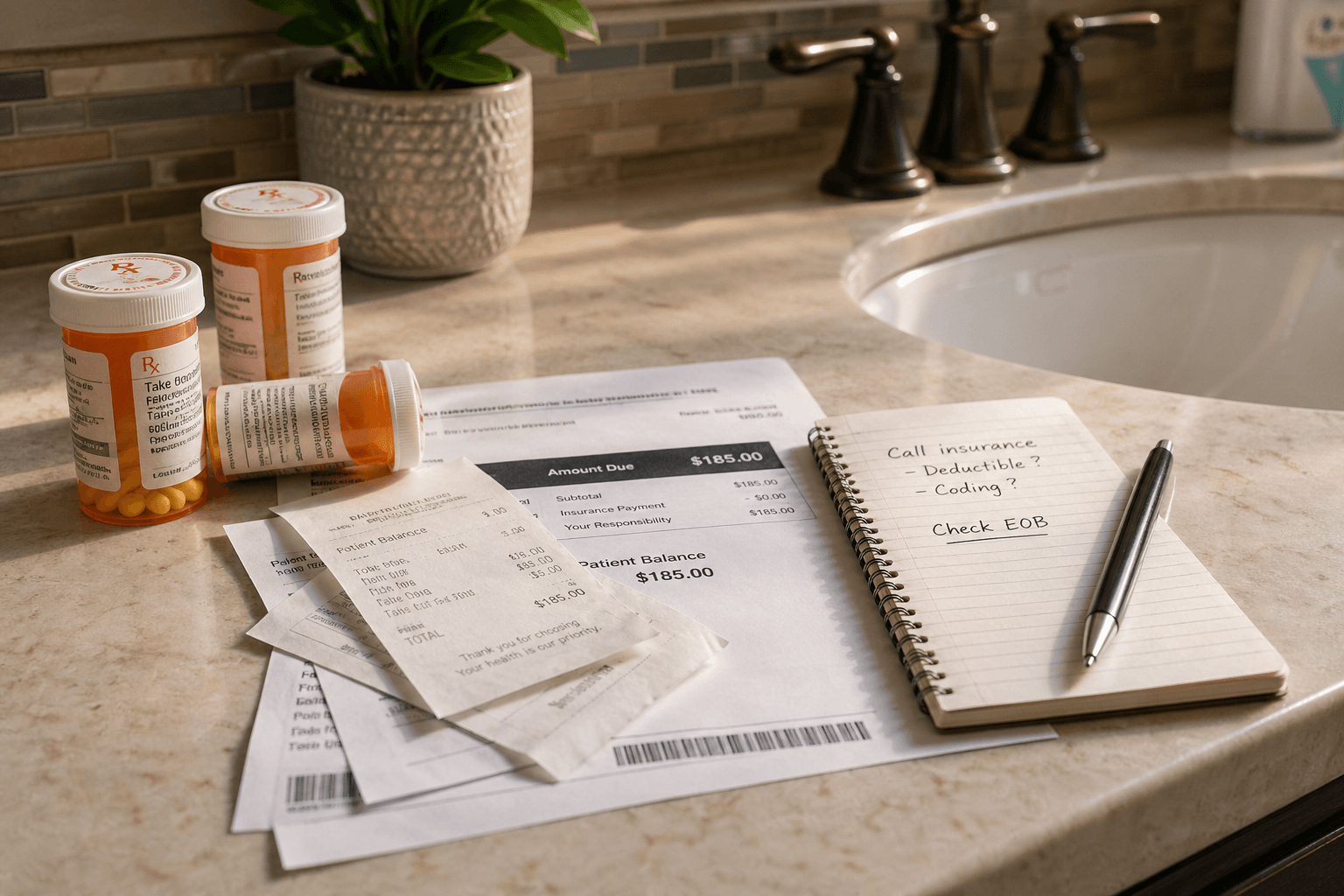

The bill didn’t look dramatically different at first. Same clinic, same doctor, same insurance card.

But the total due at checkout was $185—up from about $120 last year for what felt like the exact same visit. No major procedure. No new tests. Just a routine appointment.

That gap—small on paper, noticeable in real life—is where frustration builds. This kind of doctor visit cost increase with the same insurance is becoming more common, and it rarely comes from a single obvious change.

It’s usually the result of several small, system-level shifts quietly stacking together.

The quiet rise behind a doctor visit cost increase same insurance

Most people assume their costs should stay stable if their insurance plan hasn’t changed. In reality, costs can rise even when your plan looks identical on paper.

There are three main drivers:

1. Allowed amounts are increasing

Insurance companies renegotiate rates with providers every year. When those negotiated “allowed amounts” rise—even modestly—your share rises too.

If your plan requires 20% coinsurance, you’re paying a percentage of a higher base price.

2. Deductibles reset annually

Even if your deductible amount hasn’t changed, the reset in January matters more than most people expect.

A visit that felt like a $40 expense late last year can become a $150–$200 out-of-pocket cost early in the year before your deductible is met.

3. Service coding changes (CPT codes)

Doctors bill using CPT (Current Procedural Terminology) codes. A slightly longer visit, more detailed evaluation, or additional concern can shift your visit to a higher-level code.

From your perspective, the visit feels the same. On paper, it’s billed differently—and priced higher.

A real household example

Consider a household in Ohio:

- Annual income: $78,000

- Employer-sponsored PPO plan

- Deductible: $2,000 (unchanged)

- Coinsurance: 20%

In late 2025:

- Allowed amount: $150

- Deductible already met

- Patient paid: $30

In early 2026:

- Allowed amount: $185

- Deductible not yet met

- Patient paid: $185

Same doctor. Same plan. Completely different out-of-pocket result.

This is also where many people misunderstand their Explanation of Benefits (EOB). The EOB often shows the negotiated rate and patient responsibility clearly—but most people only look at the final bill, not how it was calculated. Situations like this often escalate into unexpected billing scenarios during routine visits, similar to what’s explained in When a Routine Doctor Visit Turns Into an Unexpected Bill: What Patients Often Miss.

What the data shows about rising outpatient costs

This pattern is backed by broader data.

According to the Bureau of Labor Statistics (BLS), physician services and outpatient care costs have shown consistent upward movement, with medical care services rising notably in recent Consumer Price Index (CPI) releases through 2024–2025.

At the same time, Federal Reserve reporting on household finances highlights that out-of-pocket healthcare spending continues to rise, especially among households enrolled in high-deductible health plans. This structure shift—where routine costs move toward the individual—is closely tied to how high-deductible health plans are reshaping everyday cash flow, as explored in How High Deductible Health Plan Upfront Costs Are Reshaping Employee Cash Flow.

The structure has shifted: insurance increasingly protects against large, unexpected events, while routine care costs are gradually pushed onto individuals.

Why the increase feels unpredictable

What makes this frustrating isn’t just the cost—it’s how disconnected it feels from the experience.

From your perspective:

- Nothing about your behavior changed

- The doctor didn’t feel more expensive

- The visit didn’t feel more complex

But behind the scenes:

- Insurers updated negotiated rates

- Billing codes (CPT) shifted slightly

- Your deductible reset

- The provider’s ownership or billing structure may have changed

This creates a system where price changes without a visible signal.

You may notice similar patterns in related areas—like routine lab work costing more at the same location, or follow-up visits being billed differently than expected. The same kind of hidden adjustment happens in income systems too, where small structural changes affect your actual cash flow, much like what’s discussed in Why Your 401(k) Contributions Quietly Increased After a Raise—and Why Your Take-Home Pay Feels Off.

Non-obvious factors most people miss

Facility ownership matters more than location

A clinic owned by a hospital system can charge facility fees—even if it looks like a standard office visit.

Preventive vs. diagnostic classification

If you mention a new symptom during a “preventive” visit, it can be reclassified as diagnostic—triggering charges.

Network complexity goes beyond your doctor

Even when your physician is in-network, labs, imaging, or specialists involved in your care may not be billed the same way.

EOB timing vs billing timing

Sometimes the bill arrives before the EOB is fully processed, making the charge feel arbitrary. Reviewing the EOB often explains the breakdown more clearly.

What this means in practice

1. The timing of care directly affects your cost

Early-year visits are usually the most expensive due to deductible resets. If the care isn’t urgent, timing can reduce out-of-pocket impact.

2. “Same insurance” does not mean stable pricing

Even without plan changes, negotiated rates and billing structures evolve every year.

3. Ask how a visit may be billed, not just what it is

A routine checkup can become a higher-cost visit depending on how it’s coded.

4. Track your deductible and EOB actively

Understanding where you stand financially within your plan prevents surprises.

5. Pay attention to provider changes—even subtle ones

A clinic acquisition or system affiliation can change billing without changing your experience.

Why this matters financially

Healthcare costs are no longer just occasional disruptions.

They’ve become a recurring, variable expense that behaves more like a fluctuating monthly bill than a fixed cost.

For many households, this leads to:

- Budget instability, especially early in the year

- Higher reliance on HSAs or savings buffers

- Occasional use of credit for routine care

It also changes behavior. Some people delay care early in the year due to cost, then cluster visits later once the deductible is met—a pattern that can affect both health outcomes and financial planning.

Understanding why your doctor visit cost increased with the same insurance isn’t just about decoding one bill. It’s about recognizing how modern health insurance distributes cost over time—and how that impacts everyday financial decisions.

FAQ

Why did my doctor visit cost more even though my copay didn’t change?

Your visit may have been applied to your deductible instead of a copay, or coded at a higher level based on services provided.

Does insurance renegotiate prices every year?

Yes. Insurers and providers regularly update contracted rates, which can increase costs without visible plan changes.

Is it cheaper to schedule visits later in the year?

Often, yes. Once your deductible is met, your out-of-pocket cost typically drops.

What should I check before paying a bill?

Review your Explanation of Benefits (EOB) first. It shows how the cost was calculated and what you actually owe.

About the Author:

Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.