By Craig R. Dunford

It didn’t happen all at once. That’s the part that makes it so disorienting.

There was no single moment — no job loss, no medical bill, no major purchase — that you can point to and say, that’s when things got tighter. The number on your direct deposit is the same it’s been for two years. Your rent hasn’t moved. Your car payment is the same. And yet somewhere between the first of the month and the fifteenth, you’re doing math you didn’t used to have to do.

This is the quiet arithmetic of everyday expenses slowly increasing over time — and it’s one of the most misread financial signals in American household life. Not because the numbers are complicated. Because they don’t announce themselves.

The Shift You Didn’t Notice Because It Never Asked Permission

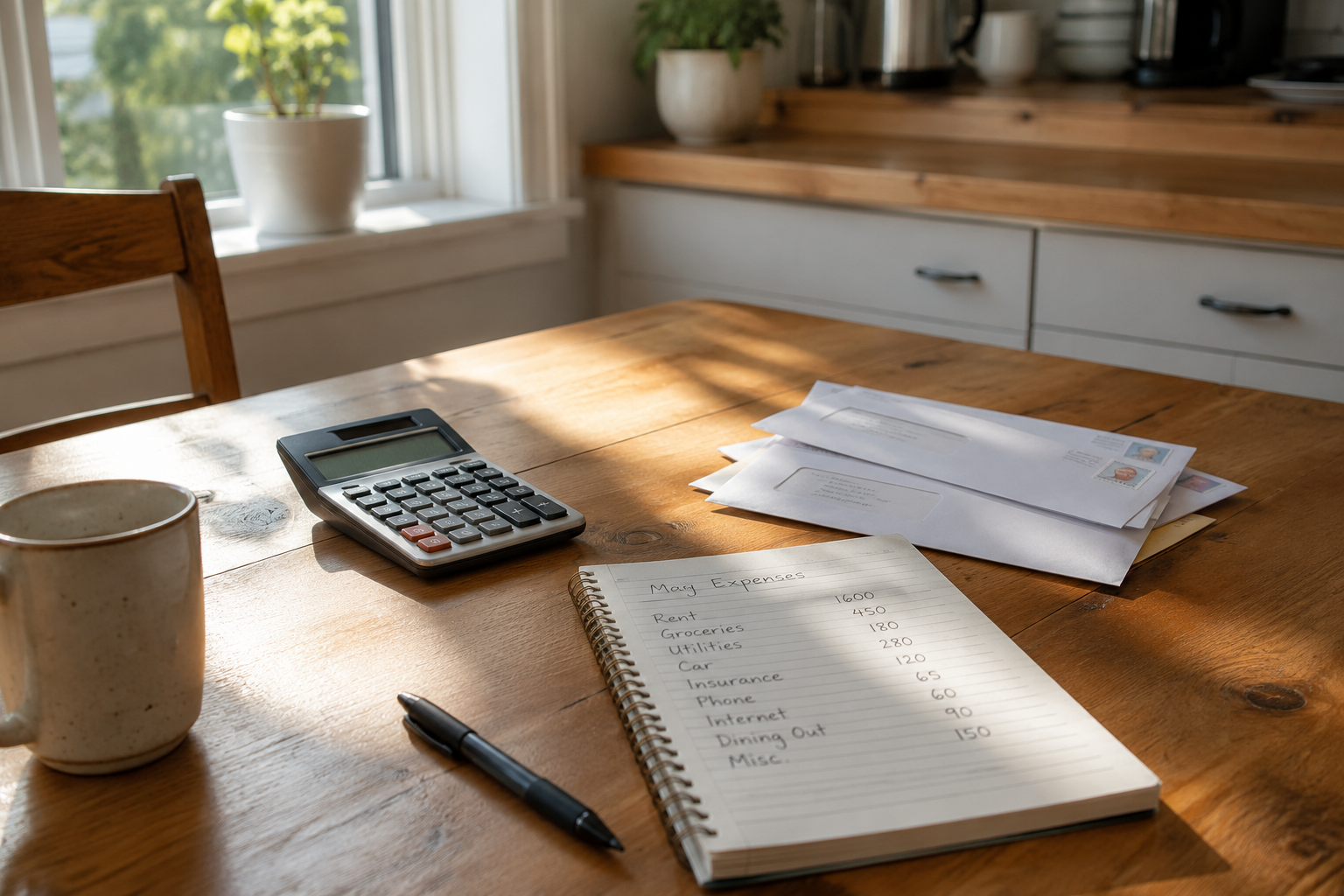

A household earning $72,000 a year — take-home around $4,400 monthly after federal and state withholding and FICA — locks in their major fixed costs. Rent: $1,350. Car payment: $415. Phone: $85. Streaming services: $47. Groceries budgeted at $520. That’s roughly $2,417 in recurring spend. Comfortable, on paper.

Then, across 18 months, the following happens without fanfare:

Their grocery bill drifts to $680. Their car insurance renews $34 higher. Their internet provider bumps the promotional rate. One streaming service goes from $15.99 to $17.99. Their electric bill averages $28 more per month due to rate adjustments they never read the notice for. Their gym membership auto-renewed at a higher tier.

No single line item breaks the budget. But the household is now spending $2,731 per month on the same life they were living for $2,417. That’s $314 extra per month — $3,768 a year — gone without a single decision being made.

This is why your paycheck feels smaller even though nothing changed. Because technically, nothing did. And that’s exactly the problem.

What the Numbers Actually Show

The Bureau of Labor Statistics Consumer Price Index has tracked persistent price pressure across core household categories — groceries, utilities, insurance, and services — over recent years. The Federal Reserve’s annual Report on the Economic Well-Being of U.S. Households (SHED report) has consistently shown that a significant share of U.S. adults report difficulty covering an unexpected $400 expense — a figure that reflects eroded margin, not just low income.

The mechanism isn’t dramatic. It’s serial. Twelve small increases across twelve different budget lines, each one survivable in isolation, collectively significant. As rising everyday costs quietly break monthly budgets for more households, this pattern repeats with enough consistency that it’s no longer an outlier — it’s a structural feature of how American household finances are being compressed right now.

Why Your Paycheck Feels Smaller: The Categories Doing the Most Damage

Not all cost increases hit the same way. Some are visible. Most aren’t.

Grocery and food-at-home costs are the most felt but the least tracked. People notice when a steak is expensive. They don’t notice when 40 individual items have each increased by 60 cents. The Bureau of Labor Statistics has documented sustained food-at-home price increases that didn’t reverse the way commodity prices sometimes do.

Auto insurance is the one most households miss until renewal. Insurance pricing works at the portfolio level — carriers adjust rates based on aggregate claims trends across their entire customer base. A driver with a spotless five-year record can still absorb a 20% premium increase at renewal because your history is one input; the carrier’s overall loss experience is the bigger one.

Subscription and service creep is different in character but equally corrosive. These aren’t dramatic increases — they’re $2 here, $4 there, an annual renewal that bumps quietly. The damage is automation: they don’t require a decision, which means they never trigger a review. A household with eight active subscriptions may be paying $60 to $90 more per month than two years ago for the exact same services.

Utility rate adjustments operate on a similar delay. Most rate changes are approved by state public utilities commissions, implemented gradually, and communicated in notices written for regulators, not households. Your bill goes up $18. You assume it’s usage. It may be a structural rate adjustment applying to every customer in your service territory.

This cost pressure doesn’t exist in isolation. The hidden costs that make experienced employees expensive — and the layoff risk that follows — is a direct consequence of the same financial squeeze hitting households and employers simultaneously.

The Delayed Realization Problem and What It Actually Costs You

The damage isn’t the cost increase itself. It’s the delay between when the erosion starts and when the household recognizes it.

Most people review their finances reactively — when something breaks, when they’re short, when a statement surprises them. By the time you notice, the pattern has often been running for 12 to 18 months. If a household was saving $400 a month and that figure quietly compressed to $140, they didn’t just lose the $260 difference — they lost it every month for a year and a half before noticing. That’s potentially $4,680 in savings that simply didn’t accumulate.

This is also why a sudden one-time expense hits harder than expected. The emergency fund didn’t build the way it was supposed to — not because the household stopped prioritizing savings, but because the monthly budget stopped working long before anyone noticed.

What This Means in Practice

Pull your last 18 months of bank and card statements and look at category totals — not individual transactions. Compare average monthly spend in groceries, insurance, utilities, and subscriptions from 18 months ago to today. The drift will be visible in a way that scanning individual transactions never shows.

Treat insurance renewals as an active financial event. Auto, renters, and homeowner premiums can increase at each renewal cycle with no change in your claims history. A brief rate comparison at renewal can recover meaningful dollars — the amount varies by carrier and region, but for many households it’s one of the highest-return uses of 20 minutes.

Build a subscription audit into your calendar once a year. List every recurring charge, its current price, and when it last increased. Anything unused in 90 days is a candidate for cancellation. Anything that increased without a corresponding improvement in value is worth cutting.

Track cost changes in dollars, not percentages. A 6% grocery increase sounds manageable. On a $650 monthly grocery spend, that’s $39 more per month — $468 per year. Dollar framing makes the actual impact legible.

The Honest Takeaway

Your paycheck is the same. The system around it isn’t.

The households that manage this well aren’t necessarily earning more. They’re the ones who review their cost structure regularly enough to catch the drift before it becomes a gap. The delayed realization is the expensive part — the longer a household runs on compressed margin without recognizing it, the harder the correction becomes.

Frequently Asked Questions

Q: At what point should I be concerned that my expenses are outpacing my income?

A: If your monthly savings rate has declined by more than 30% over 12 to 18 months without a clear life change — new dependent, housing move, medical event — run a category-by-category comparison against your spending from 18 months prior. A drift of $200 to $400 per month across fixed and semi-fixed costs is more common than most households realize.

Q: When is the best time to review recurring costs and subscriptions?

A: Annually, timed around your insurance renewal dates. Build your full recurring cost review around that date — it creates a natural forcing function to evaluate all fixed costs together rather than piecemeal.

Q: How does system-level inflation actually reach my household budget?

A: Through two channels. The first is direct — grocery prices, utility rates, goods at the point of sale. The second is indirect — service providers, insurers, and landlords adjust their own costs upward and pass increases to customers on their own schedules, often out of sync with headline CPI numbers. This is why household budgets frequently absorb the full weight of an inflationary period 12 to 24 months after economists declare it over.

Q: Is it possible my take-home pay actually changed without me noticing?

A: Yes. Federal withholding adjusts based on W-4 elections, and any change in filing status or employer payroll systems can shift net pay. Social Security withholding — 6.2% of wages — applies up to the annual wage base ($168,600 for 2024), stops when earnings cross that threshold mid-year, and resets automatically on January 1. Pulling three consecutive pay stubs and comparing deduction line items is the fastest way to confirm.

About the Author

Craig R. Dunford covers U.S. personal finance, household income behavior, and tax strategy for Wealth Power. His analysis draws on Federal Reserve publications, IRS data, and nearly a decade of tracking financial patterns across American households.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Individual financial situations vary. Readers should consult a qualified financial, tax, or legal professional before making any financial decisions.