Last Updated: April 2026

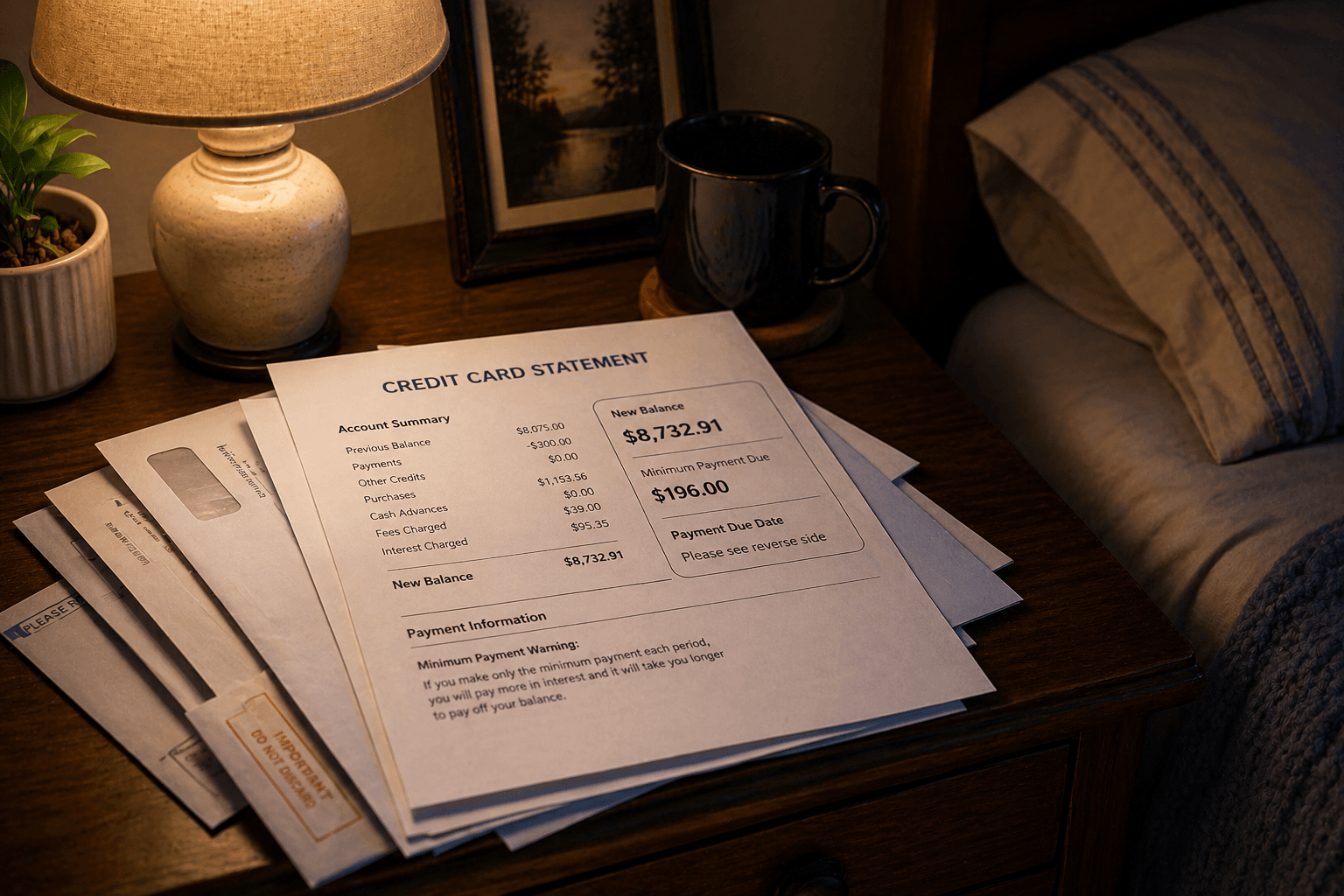

Every January, the numbers look clean again. New year, fresh budget, and a decision to finally get ahead on credit cards. You start paying more than the minimum. Yet by March or April, the balance is somehow higher than where you started.

That disconnect—credit card balance growing despite payments—is not random. It’s a structural issue tied to how income, expenses, and revolving credit interact.

The income–expense gap most people underestimate

For many U.S. households, the problem isn’t irresponsible spending. It’s a quiet mismatch between income timing and real expenses.

Consider a household earning $5,200/month after taxes:

- Rent: $1,800

- Groceries: $700

- Car + insurance: $650

- Utilities + subscriptions: $400

- Childcare: $900

- Miscellaneous (fuel, medical, school, etc.): $600

Total: $5,050

On paper, they still have $150 left. So they pay $300 toward their credit card, assuming they’re making progress.

But the missing piece is variability.

A single unexpected cost—a $400 car repair or a seasonal spike in electricity—gets pushed onto the credit card. That erases the progress instantly. Over time, this creates a net inflow of new debt, even while payments increase.

According to the Federal Reserve Bank of New York’s Household Debt and Credit Report, U.S. credit card balances have exceeded $1.1 trillion in recent periods—reflecting not just spending, but persistent rollover balances driven by these mismatches. In many cases, this pressure builds alongside rising fixed costs, particularly housing, as explained in Property Tax Increases Are Quietly Raising U.S. Housing Costs.

Why credit card balance growing despite payments is structurally normal

Credit cards are designed around compounding and timing, not fairness.

Even if you pay more than the minimum:

- Interest accrues daily, not monthly

- New purchases often start accruing interest immediately if you carry a balance

- Payments are applied based on issuer rules, which may not reduce your highest-cost balance first

If your APR is 22% and your balance is $8,000, you’re paying roughly $140–$150/month in interest alone.

If you pay $300:

- ~$150 goes to interest

- Only ~$150 reduces principal

Now add $200 in new charges during the month. You’ve effectively gone backward.

This is where many people misread progress. The payment amount feels meaningful, but the net balance movement is what actually determines whether you’re getting out of debt.

The hidden layer: debt stacking across billing cycles

What often goes unnoticed is how billing cycles create “layered debt.”

You’re not just paying off one balance. You’re dealing with:

- Previous cycle balance (already accruing interest)

- New charges (often interest-bearing immediately)

- Timing gaps between statement closing date and payment date

This creates a rolling effect where:

- You reduce part of the old balance

- New charges refill the balance before the next cycle closes

- Interest continues compounding across both layers

Over time, this produces a payment lock-in effect—your monthly payment stabilizes, but your balance doesn’t drop in a meaningful way.

It’s a pattern similar to cost-of-living creep or paycheck mismatches, where small misalignments quietly compound—something many workers notice when Why U.S. Paychecks Feel Smaller Despite Stable Salaries becomes a lived reality.

Why Paying More Still Doesn’t Reduce Your Credit Card Balance

There’s a common assumption: “If I just pay more, I’ll eventually catch up.”

That only works if your net cash flow is consistently positive after all expenses.

If your real monthly expenses exceed income—even slightly—you’re structurally dependent on credit.

Increasing payments without fixing that gap does two things:

- It tightens short-term cash flow

- It pushes more day-to-day spending back onto the card

This creates a loop:

Higher payment → less available cash → more card usage → higher balance

At that point, the issue isn’t discipline—it’s system design. Many households reach a point where they feel like they’re doing everything right—and still falling behind, especially during periods when variable income like bonuses underperform expectations, as explored in Why U.S. Bonuses Feel Smaller Than Expected.

What this means in practice

- Track net balance change, not payment size

Focus on whether your total balance is declining month over month—not just how much you’re paying. - Separate spending from repayment periods

If possible, stop using the same card you’re trying to pay down. Mixing both hides the real progress. - Calculate your true monthly surplus or deficit

Even a $75–$100 shortfall can quietly keep balances rising over time. - Time payments within the billing cycle

Paying earlier reduces your average daily balance, which directly lowers interest. - Audit “invisible” expenses every few months

Subscriptions, insurance adjustments, and irregular bills often drive the gap—not obvious spending.

The deeper financial signal most people miss

When a credit card balance grows despite payments, it’s rarely about the card itself.

It’s a signal that:

- Income hasn’t kept pace with real living costs

- Expense volatility isn’t being absorbed by savings

- Credit is functioning as a liquidity tool, not just borrowing

Warning signal: If your balance hasn’t decreased over 3–4 billing cycles despite consistent payments, you are likely operating in a negative cash flow loop—not making real progress on debt.

This is why many households feel financially stuck even when doing the “right” things.

You’re not just managing debt—you’re offsetting a structural cash flow imbalance.

FAQ

Why does my balance increase even when I pay twice the minimum?

Because interest and new charges can exceed your principal reduction. If your net monthly change is positive, the balance will grow regardless of payment size.

Should I stop using my credit card completely?

If you’re carrying a balance, temporarily pausing usage can help you isolate repayment and make measurable progress.

When is the best time to make a payment?

Earlier in the billing cycle reduces your average daily balance, which lowers interest. Waiting until the due date allows more interest to accrue.

Is this a budgeting issue or an income issue?

Often both, but primarily a cash flow mismatch. If expenses consistently exceed income, budgeting alone won’t solve it—you may need to adjust expenses or increase income.

Conclusion

A growing credit card balance despite steady payments isn’t a failure of effort—it reflects a mismatch in how money flows through your system.

Until that gap is addressed, payments will feel productive, but the balance will continue to tell a different story.

About the Author:

Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.