You get the raise email. The new salary looks solid on paper. But when the next paycheck hits your account, something feels off. The number isn’t meaningfully higher—and in some cases, it’s barely different at all.

That disconnect isn’t a payroll error. It’s the way your paycheck is structured.

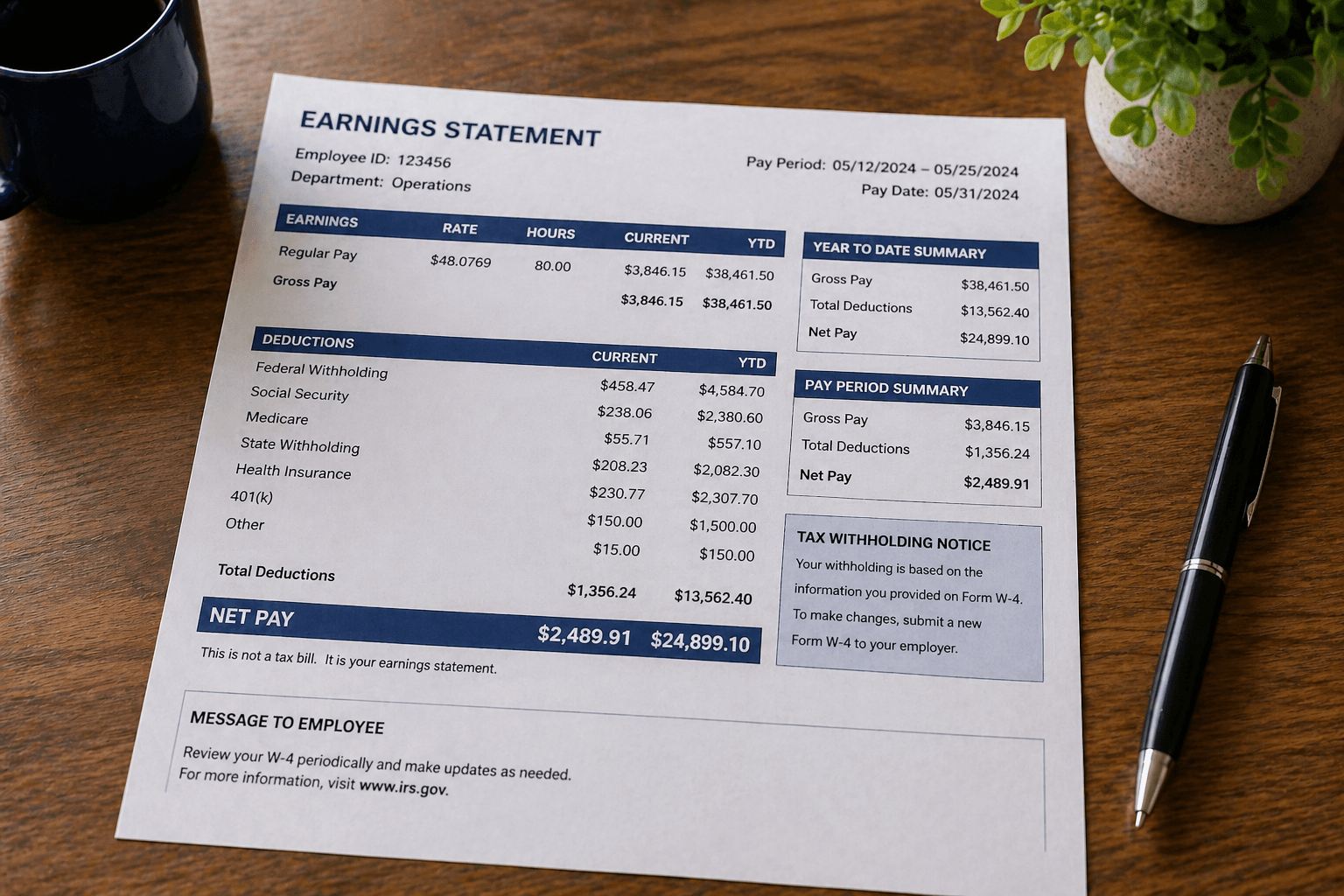

Understanding why paycheck smaller after raise taxes comes down to how your income flows through withholding, taxes, and benefits—not just how much you earn on paper.

For many workers, this confusion becomes even sharper when raises stop keeping pace with real expenses—something explored in why annual raises no longer cover rising living costs for W-2 workers. The paycheck doesn’t just reflect income—it reflects pressure from multiple directions.

The hidden billing structure inside your paycheck

A paycheck isn’t just income minus tax. It’s a layered system of deductions that respond differently when your salary increases.

Here’s what typically changes after a raise:

- Federal income tax withholding increases (based on W-4 settings)

- State taxes adjust proportionally

- Payroll taxes (Social Security and Medicare) apply to higher wages

- Employer benefits—like health insurance or retirement contributions—may scale with salary

Each of these acts like a separate “billing line item.” When your income rises, multiple deductions expand at once.

The result is subtle but important: your raise gets distributed across these systems before it reaches your bank account.

What most people don’t realize is that payroll systems are designed for consistency, not precision. They assume stable income patterns—even when your actual earnings change mid-year.

Why paycheck smaller after raise taxes becomes noticeable

The confusion usually comes from how withholding works—not your actual tax bill.

The IRS operates on a pay-as-you-go system, where your employer estimates taxes per paycheck using W-4 inputs and current earnings. When your income jumps, the system often assumes that higher level applies consistently across the year.

That leads to a few effects:

- Withholding may increase more aggressively than expected

- Only the additional income is taxed at a higher marginal rate—but withholding can make it feel like your entire income is

- Bonuses or irregular pay increases are often withheld at flat rates (commonly 22% federal), which can distort expectations

A key distinction: your marginal tax rate applies only to the top portion of income, while your effective tax rate is much lower. The paycheck system doesn’t always make that difference obvious.

This becomes more noticeable in mid-career stages, where income grows but financial acceleration slows—a pattern closely tied to why career growth quietly slows after mid-career.

This is why the increase feels smaller—it’s not just taxes, it’s how taxes are being collected in advance.

A real household example with numbers

Consider a dual-income household in Texas:

- Previous salary: $75,000

- New salary after raise: $85,000

- Pay frequency: biweekly

Before the raise:

- Gross paycheck: ~$2,885

- Federal withholding: ~$350

- Social Security & Medicare: ~$220

- Benefits (health + 401(k)): ~$400

- Net: ~$1,915

After the raise:

- Gross paycheck: ~$3,269

- Federal withholding: ~$450

- Social Security & Medicare: ~$250

- Benefits (health + 401(k) increased contribution): ~$520

- Net: ~$2,049

The raise adds about $384 to gross pay per paycheck—but only ~$134 shows up as additional take-home income.

Where did the rest go?

- ~$100 absorbed by higher federal withholding

- ~$30 more in payroll taxes

- ~$120 redirected into benefits and retirement contributions

Nothing “disappeared.” It was reallocated across systems that automatically scale with income.

This is also where many households begin to feel a quiet budget strain—not because income is falling, but because it’s not stretching as expected, similar to what’s described in you don’t notice the cost of living creep until your monthly budget stops working.

Benefit deductions quietly scale with income

One of the least obvious reasons your paycheck feels smaller is how benefits behave in the background.

Many employees increase their 401(k) contributions after a raise—sometimes intentionally, sometimes through auto-escalation features tied to compensation changes. Even a small percentage increase can noticeably reduce take-home pay.

Healthcare costs can shift too:

- Premium tiers may change during open enrollment

- Employers may adjust cost-sharing year to year

- FSA or HSA contributions often increase alongside income planning

According to the Bureau of Labor Statistics, benefits make up roughly 30% of total compensation in the U.S. That means a meaningful portion of any raise may never show up as cash—it’s being redirected into longer-term or non-cash value.

There’s also a compounding effect here. When contributions rise alongside income, your financial position may improve on paper (higher savings, better coverage), but your immediate liquidity tightens.

The psychological mismatch between salary and take-home pay

A raise is communicated as an annual number. But your financial life runs on what lands in your account every two weeks.

That gap creates a perception problem:

- You think in annual salary

- You experience income in net pay

When multiple deductions increase at once, the raise feels diluted—even if your overall compensation improved.

There’s also a timing effect that often goes unnoticed:

- Raises frequently happen mid-year

- Withholding systems assume consistency across the full year

- This can temporarily increase withholding beyond your actual tax liability

Many people don’t revisit their W-4 after a raise, so the system keeps operating on outdated assumptions. Over time, that can lead to either a refund or an unexpected adjustment.

What this means in practice

- Review your W-4 after any salary change

Use the IRS Tax Withholding Estimator or reference IRS Publication 15-T to better align withholding with your actual liability - Separate tax impact from benefit choices

If your net pay barely changed, check whether increased retirement contributions or benefit elections are driving the difference - Expect marginal—not proportional—growth in take-home pay

A raise improves income, but not in a one-to-one way at the paycheck level - Track net pay, not just salary

Your spending and saving decisions should be based on actual cash flow, not gross income - Be cautious with automatic contribution increases

Increasing 401(k) contributions is valuable—but doing it without adjusting your budget can create short-term cash pressure

Conclusion

Your paycheck isn’t shrinking after a raise—it’s being redistributed across taxes, benefits, and withholding systems that adjust with your income.

Once you understand how each layer works, the numbers stop feeling inconsistent. The raise is real—but it shows up differently than most people expect.

FAQs

Why does my paycheck increase so little after a raise?

Because multiple deductions scale at once—tax withholding, payroll taxes, and benefits all increase, reducing the visible impact on net pay.

Am I paying more taxes than I should after a raise?

Not necessarily. You may be over-withholding temporarily. Your actual tax liability depends on total annual income, not per-paycheck estimates.

Should I change my W-4 after getting a raise?

In most cases, yes. A raise can misalign your withholding. Updating your W-4 helps prevent overpaying or underpaying taxes.

Do bonuses and raises get taxed the same way?

No. Bonuses are often withheld at a flat federal rate (typically 22%), while regular salary is withheld based on W-4 calculations, which can lead to different paycheck outcomes.

About the Author:

Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.