The number shows up before the explanation does.

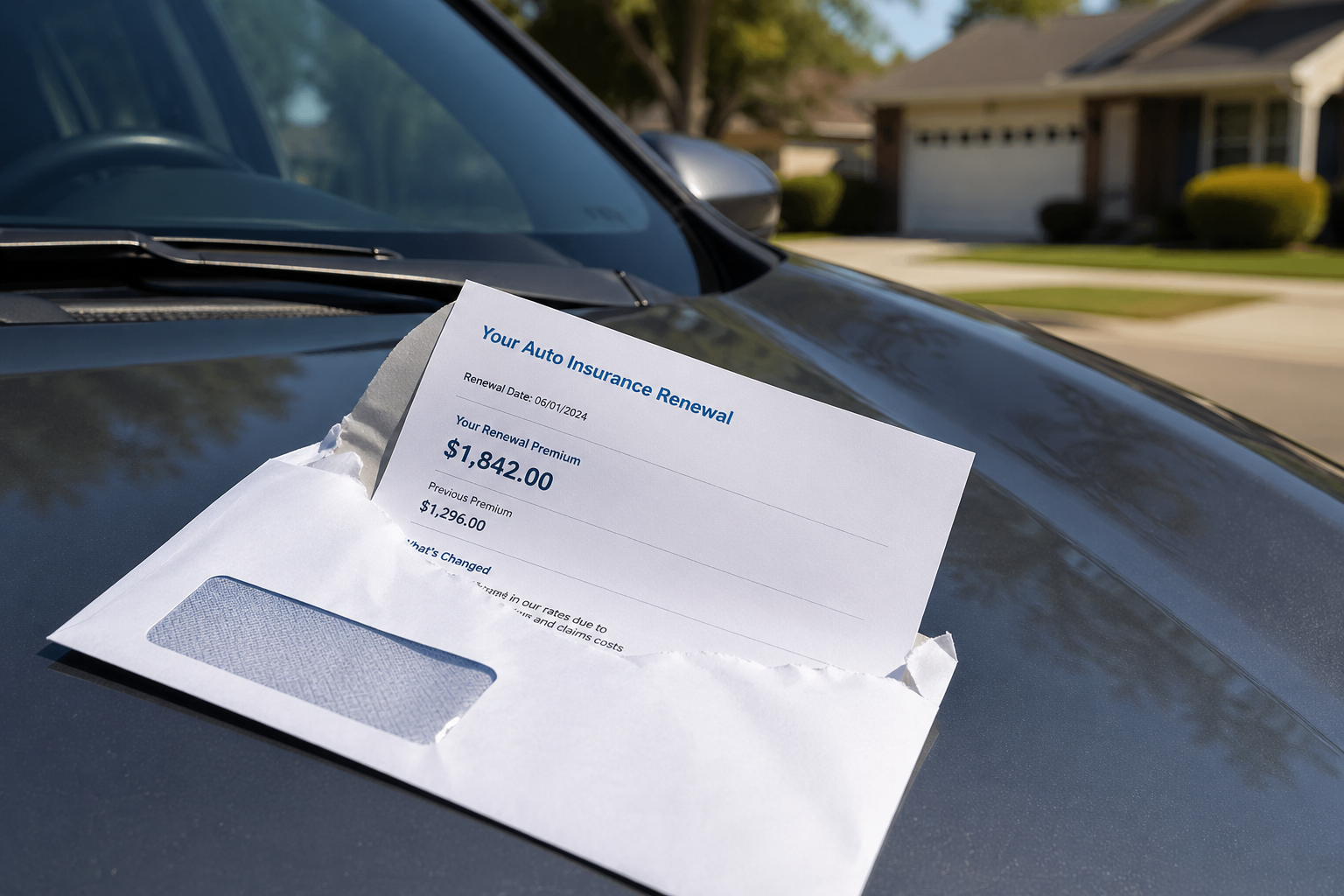

$1,842 for six months. Last cycle was $1,296.

Same car. Same driver. No accidents. No tickets.

And yet, the renewal notice quietly reflects a car insurance premium increase renewal reason that isn’t tied to anything you did—but very much tied to when your policy renewed.

The renewal timing problem most drivers miss

Insurance pricing doesn’t move gradually—it resets in chunks.

When your policy renews, the insurer recalculates your risk based on current market conditions, not your past behavior alone. That timing matters more than most people realize.

Between renewals, insurers absorb changes in claim costs, repair inflation, and regional risk trends. But at renewal, all of that gets applied at once.

In 2024, the Bureau of Labor Statistics reported that motor vehicle insurance costs rose over 20% year-over-year, one of the sharpest increases in decades. That surge didn’t hit everyone at the same time—it hit when their policies renewed.

Adding to this, insurers don’t change rates freely. In most states, they must file for approval with regulators before adjusting premiums. Once approved, those new rates roll out across renewal cycles—not instantly. That delay is exactly why timing creates uneven outcomes.

So if your renewal landed during a high-cost recalibration window, your premium jumped—even if your personal risk didn’t.

What actually changed behind the scenes

Most premium increases without claims come from system-level adjustments, not individual ones.

Here’s what insurers quietly updated:

1. Repair cost inflation

Modern vehicles are expensive to fix. Sensors, cameras, and advanced materials mean even minor accidents cost more. Insurers adjust premiums based on projected repair costs—not your driving record.

2. Regional risk recalibration

If accident frequency, theft rates, or litigation costs increased in your ZIP code, your risk profile changed—regardless of your behavior.

3. Reinsurance costs rising

Insurance companies themselves buy insurance (reinsurance). When those costs rise due to large-scale losses (like hurricanes or wildfires), the increase flows downstream to policyholders.

4. Claims severity—not just frequency

Even if accident rates stabilize, the cost per claim has been rising. According to industry data from the National Association of Insurance Commissioners (NAIC), severity has been a key driver of premium adjustments in recent years.

None of these show up as “your fault,” but all of them show up on your bill.

Car insurance premium increase renewal reason: why timing drives the spike

The key issue isn’t just why your premium increased—it’s when.

Insurance pricing works on cycles. If your renewal happened:

- Right after a major industry-wide rate filing approval

- During a period of high claims payouts

- After inflation-adjusted recalculations

…you absorbed the full adjustment immediately.

Another driver renewing three months earlier might still be on older pricing. Someone renewing three months later might face an even higher rate.

This creates a timing gap where identical drivers pay very different premiums.

This same timing effect shows up across policies, which is explored further in why your insurance premium jumps right after renewal even when nothing changed, where renewal cycles—not behavior—drive sudden cost shifts.

A real household example

Take a two-driver household in Ohio:

- 2019 Honda CR-V

- Clean driving record

- Previous premium: $1,150 (6 months)

At renewal, their premium jumped to $1,520.

No claims were filed.

What changed?

- Local repair costs increased ~15% due to parts shortages

- Regional accident severity rose post-pandemic (more high-speed collisions)

- Insurer updated pricing models during that quarter

- A state-approved rate increase took effect just before their renewal date

Their risk didn’t change. The timing of their renewal aligned with cost recalibration.

That’s the hidden layer most drivers never see.

The behavioral trap: assuming stability means price stability

Many drivers believe:

“No claims = no increase.”

That assumption doesn’t hold in insurance markets.

Insurers price for future risk, not past behavior. And future risk is constantly being re-evaluated based on external data.

This creates a disconnect:

- You experience stability

- The system experiences volatility

And at renewal, the system wins.

In some cases, this mismatch leads people to delay reviewing their policies—assuming loyalty or a clean record will stabilize costs. In reality, similar patterns show up in other areas, like why my credit card balance keeps growing even though I pay more than the minimum each month, where the system mechanics override what feels like “correct” behavior.

What this means in practice

1. Renewal timing matters more than loyalty

Staying with the same insurer doesn’t protect you from pricing resets. Shopping around just before renewal can reveal whether your increase is market-wide or company-specific.

2. Small coverage changes can offset timing shocks

Adjusting deductibles, reviewing collision coverage on older vehicles, or bundling home and auto can soften sudden increases.

3. Your ZIP code is quietly driving your premium

Even without moving, local risk shifts can impact your rate. This mirrors what happens in healthcare billing, as seen in why your doctor visit cost more this year even with the same insurance plan, where underlying cost structures change despite stable coverage.

4. Inflation hits insurance in waves, not gradually

Unlike everyday expenses, insurance adjusts in discrete jumps. That’s why increases feel sudden rather than incremental.

5. Your next renewal may not behave the same way

If cost pressures stabilize or fewer rate filings are approved, your next cycle could level off.

Why this matters beyond one bill

This isn’t just about one renewal—it reflects how modern insurance pricing works.

Premiums are no longer tightly tied to individual behavior. They’re shaped by aggregated risk, predictive modeling, regulatory approvals, and cost forecasting.

That’s why many households feel blindsided—even financially responsible ones.

Understanding this pattern also makes it easier to interpret other financial shifts. Rising HOA fees, healthcare premiums, or even utility pricing often follow the same structure: long periods of stability followed by sudden resets.

Conclusion

Your premium didn’t increase because you became a worse driver.

It increased because your renewal landed at a moment when the system recalculated risk—and applied it all at once.

Once you see that timing layer clearly, the number on your bill stops feeling random—and starts making sense.

FAQs

Why did my car insurance go up if I didn’t file a claim?

Because insurers adjust rates based on overall risk trends, repair costs, and regional data—not just individual claims history.

Is it better to switch insurance right after a renewal increase?

Often yes. That’s when you can compare whether your increase reflects the broader market or your insurer’s pricing model.

Do insurance rates go down if industry costs drop?

They can, but usually with a delay. Rate decreases tend to follow sustained cost reductions, not short-term changes.

How often do insurers recalculate premiums?

Typically at each renewal period (every 6 or 12 months), based on updated underwriting models, regulatory approvals, and market data.

About the Author:

Wealth Power Editorial Desk focuses on U.S. personal finance patterns, including taxation, income structure, and behavioral finance. Content is built on structured analysis and real-world financial observations.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Readers should consult a qualified professional before making financial decisions.